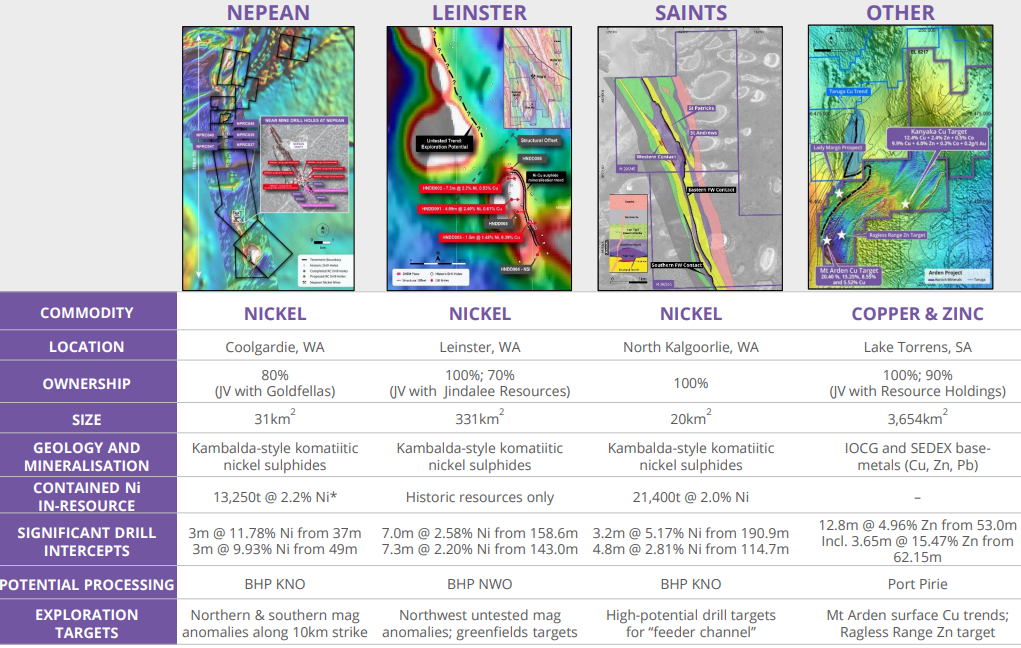

Auroch Minerals Ltd (ASX: AOU) is a nickel sulphide focused base-metal resource company building value through targeted high-impact exploration in Western Australia.

AOU has three nickel projects in Western Australia, one of the world’s richest regions for nickel sulphides.

AOU’s nickel projects all sit in the Norseman-Wiluna Greenstone Belt, home to some of the best nickel projects globally including Leinster, Mt Keith, Kambalda and Widgiemooltha.

All of AOU’s projects, including Leinster and Saints are highly prospective for near surface, high grade nickel sulphide mineralisation.

The Nepean Nickel Project is AOU’s primary focus.

The Nepean Nickel Project contains the historic high-grade Nepean nickel sulphide mine. There are several highlights:

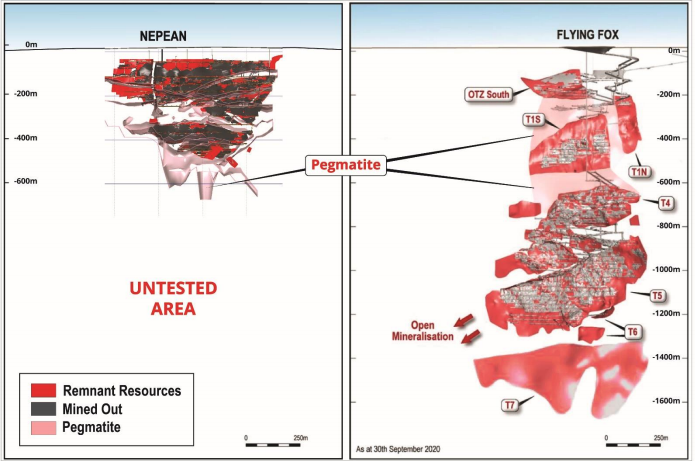

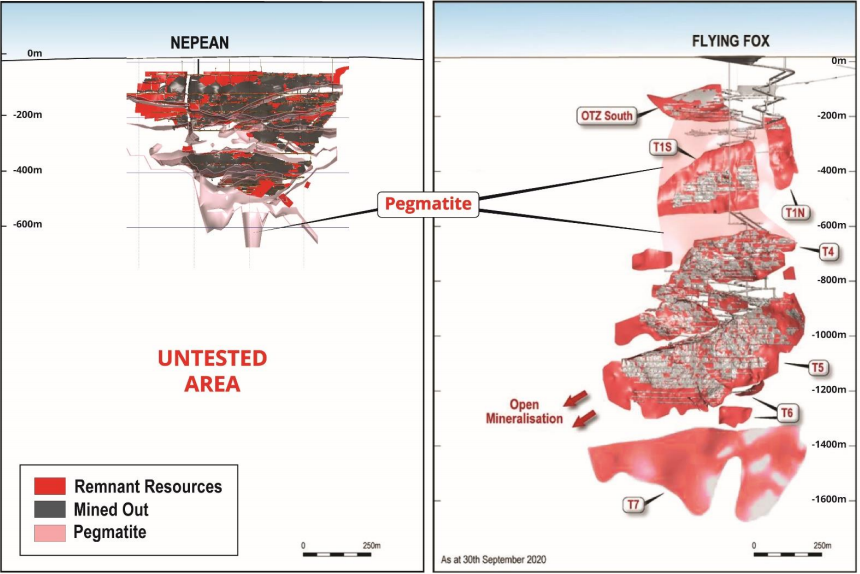

You can see the comparison between Nepean and Flying Fox below:

The question now is whether Nepean can become another Flying Fox.

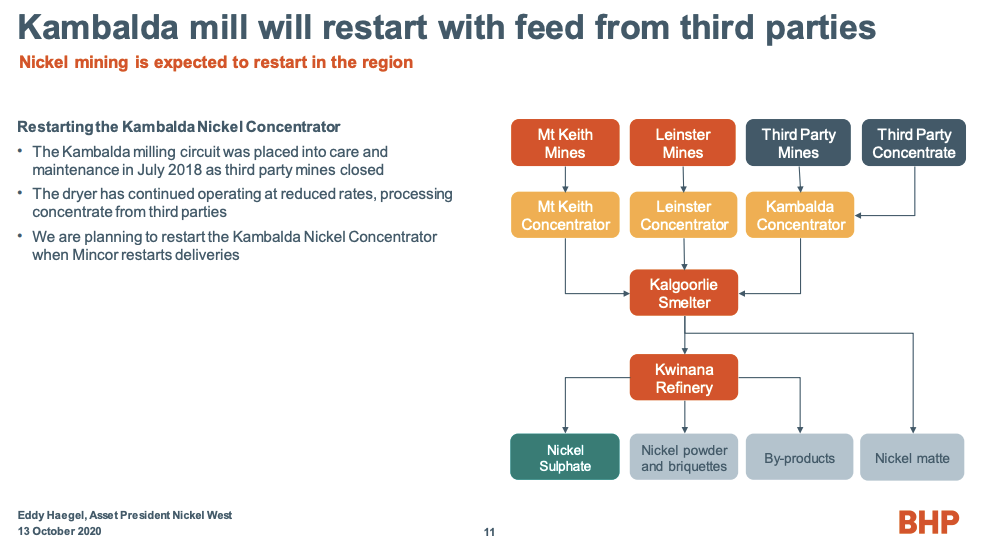

One further highlight is Nepean is 70km from BHP’s Kambalda Nickel Concentrator and Smelter.

Late last year, BHP announced it would be establishing itself as a primary supplier of materials to the battery and electric vehicle markets. In doing so, the company confirmed that it was boosting nickel production in response to Tesla CEO Elon Musk calling for miners to ramp up output of the key material used in the company’s batteries.

The presence of nearby processing facilities operated by third parties, including BHP’s Kambalda smelter, is a substantial benefit for AOU as BHP looks for more nickel supply.

We see multiple share price catalysts on the horizon for AOU:

The key reasons for us choosing to invest in AOU are:

AOU entered into a binding agreement to acquire 80% of the shares in Eastern Coolgardie Goldfields Pty Ltd (ECG), the company that will hold the Nepean Nickel Project, comprising a package of 13 tenements located 25 kilometres south of Coolgardie, in Western Australia.

Following the acquisition of the remaining 20% by Goldfellas Pty Ltd, AOU and Goldfellas will operate the Nepean Nickel Project as a joint venture with AOU holding an 80% participating interest and Goldfellas the remaining 20%.

The Nepean Nickel Project contains the historic high-grade Nepean nickel sulphide mine, which was the second producing nickel mine in Australia, producing just over 1.1 million tonnes of ore between 1970 and 1987 for about 32,200 tonnes of nickel metal at an impressive average recovered grade of 2.99% nickel.

The ore was treated by Western Mining Corporation (WMC, now BHP Group Ltd) at its Kambalda processing facilities which is still in operation.

The Nepean mine closed in 1987 due to low nickel prices, leaving significant nickel sulphide resources unmined.

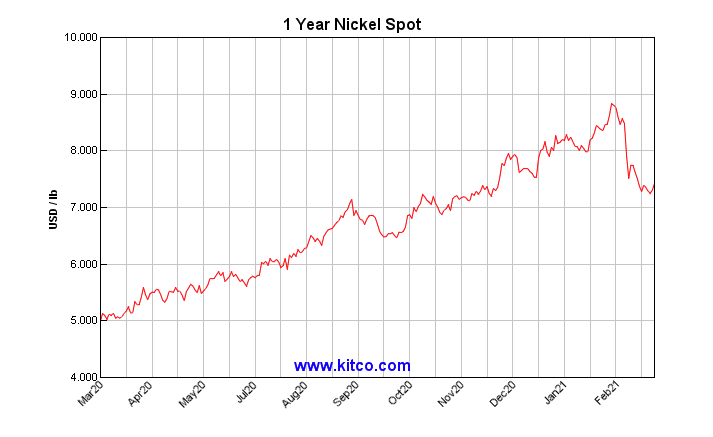

And low was very low. At the end of 1986 when a fight or flight decision had to be made, the nickel price was hovering in the vicinity of US$1.60 per pound, about 80% below current levels.

Times have now changed with the nickel price now at over US$7.00 per pound.

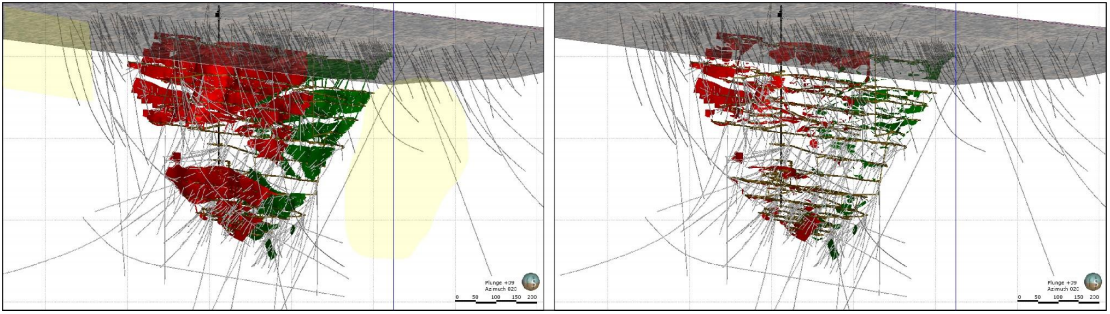

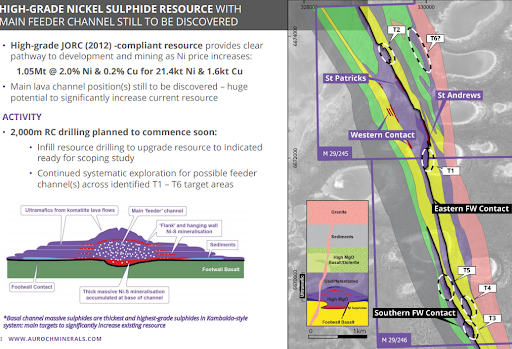

The nickel sulphide mineralisation in the Nepean mine is typically massive to semi-massive sulphides with a very high nickel tenor, contained predominantly in two main bodies, Sill 2 (red) and Sill 3 (green) as shown below.

While this gives you an idea of the known, it is more the unknown that intrigues Wise-Owl because what you see above may just be the tip of the iceberg.

The following diagram shows a comparison with Western Area’s Flying Fox mine (right side) which is regionally relevant and bears many similarities in terms of mineralisation and structure.

Most significantly, just like Nepean, Flying Fox was constrained by pegmatites at a relatively shallow depth. Flying Fox was constrained at around 300 metres and then at a deeper level of approximately 600 metres, with the latter being consistent with the depth and positioning of the pegmatite below the orebody at Nepean.

As you can see above, deeper drilling at Flying Fox unveiled substantial open mineralisation below the pegmatite wide zones between about the 700 metre and 1200 metre mark.

In addition to the near-mine prospectivity, management believes that Nepean has enormous potential to host further significant nickel sulphide mineralisation, with the 3,128 hectare tenement package hosting over 10 kilometres of underexplored strike of the Nepean mafic-ultramafic mine stratigraphy and/or aeromagnetic anomalies.

The company has identified several high-priority areas, and a 3,500 metre reverse-circulation (RC) drill programme has already yielded some extremely promising results including 3 metres at 3.7% nickel, including 2 metres at 5.1% nickel, as well as one metre at 5.6% nickel.

Two lenses of high-grade massive nickel sulphides, each up to 6 metres thick have now been defined at depths of less than 100 metres for more than 500 metres of strike. All intersections to date have also identified some copper mineralisation.

Twenty drill-holes have been completed for approximately 2,400 metres of the maiden drilling programme at Nepean, comprising 10 shallow near-mine drill-holes and 10 regional drill-holes testing aeromagnetic targets along the 10 kilometres of prospective strike.

With plenty more drilling results to filter through in the coming weeks, there are plenty of catalysts investors can look forward to.

Looking beyond this drilling program, management expects to complete a resource estimate by year-end, enabling it to fast track Nepean to production.

Previous mining has pointed to the prospect of gold and lithium mineralisation, and management will be on the lookout for similar occurrences, though the key focus is on the project’s nickel-copper prospectivity.

Towards the end of February this year, nickel hit a near seven-year high as it pushed up towards the psychological US$9.00 per pound mark.

However, as you can see from the chart above, since the start of March the metal has fallen by approximately US$1.00 per pound as concerns arose regarding oversupply from a potential decision by Indonesia that would allow for a restoration in nickel ore exports after a three-year ban.

With these dynamics in play, speculative selling is occurring, effectively boosting inventories.

However, most analysts are of the view that equilibrium will return.

Tesla chief executive Elon Musk commented that nickel was the company’s “biggest concern” in scaling lithium-ion cell production.

Nickel is one of the priority metals in the manufacture of Tesla’s batteries and the car giant is looking to increase its nickel supply.

There may also be some direct investment from other auto manufacturers who have expressed a desire to move to a vertically integrated model whereby they have better control over the supply chain in relation to commodity inputs.

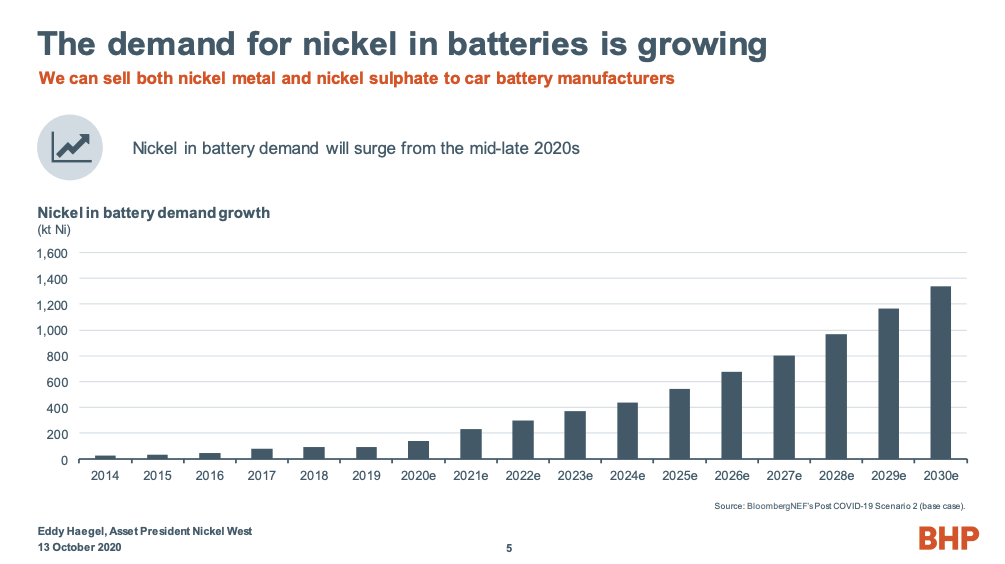

From a longer term perspective, analysts are generally expecting tailwinds for the nickel price due to increasing demand from the electric vehicle industry. The World Bank predicts that Nickel demand is guaranteed to increase by some of the most dramatic figures by tonnes.

This would be good news for AOU in the long-term.

It would appear that both new supply and a loosening in trade barriers are required to meet the uptick in demand.

While there has been much talk of changes in battery manufacturing, as recently as two weeks ago Volkswagen held its Power Day, reaffirming that lithium, manganese and nickel would be the key commodities used across its battery range.

With regard to supply chain management, Jorg Teichman, VW’s Chief Purchasing Officer said that the group plans to expand the scope of its value chain from purchasing of raw materials directly from miners to making investments in various parts of the supply chain.

Volkswagen declared they will be raising the amount of Nickel used in their electric car battery cells to 80% from current 65% in the next year: moving from 65% Nickel, 15% cobalt and 20% Manganese, to 80% Nickel, 10% Cobalt and 10% Manganese. This is across all their brands including Porsche, Audi and Scania.

Volkswagen is targeting 3 million EVs by 2025, and will be sourcing green Nickel Sulphide from sustainable mines.

As battery metals stocks are seeing a massive surge in investor demand, nickel explorers like AOU that are located in highly prospective regions and in close proximity to established production hubs are likely to attract investor attention on the back of the current surge in nickel demand.

Not only will a company such as AOU be viewed as potentially being able to bring new production to the likes of BHP to coincide with the uptick in nickel demand, but it will also be viewed as a potential takeover target by mid-tier players looking to establish a hub and spoke strategy, or multiple sources of additional feedstock for one of the majors like BHP.

Last year, BHP Nickel West asset president Edward Haegel mentioned the possibility of Tesla using BHP’s nickel supply, of which 70 per cent is already used to develop batteries around the world.

Speaking at the Diggers and Dealers forum in Kalgoorlie, asset president for BHP’s Nickel West subsidiary, Eduard Haegel, said calls by Tesla’s Elon Musk for more nickel production highlighted the scale of opportunity being created by the clean energy sector for materials, but stopped short of confirming that BHP had finalised a nickel supply deal with Tesla.

However, Haegel did say, “Nickel West is well positioned to benefit from this anticipated growth. Last year, we sold around 70 per cent of our nickel to battery manufacturers around the world, making BHP one of the world’s leading battery metal suppliers.”

In July last year, Musk said that a “giant contract for a long period of time” would be provided to a miner capable of sustainably extracting nickel due to the high cost of EV batteries.

Musk has confirmed that Tesla already sources lithium from Australia, and it was reported last year that Tesla and BHP were in confidential discussions as the former went public in saying that it is looking to improve battery performance through increased use of nickel in battery production.

While Musk has backtracked in recent days, overall activity in the sector including from VW and statements from billionaire investor Chamath Palihapitya and the World Bank, suggest that the requirement for nickel will continue to increase.

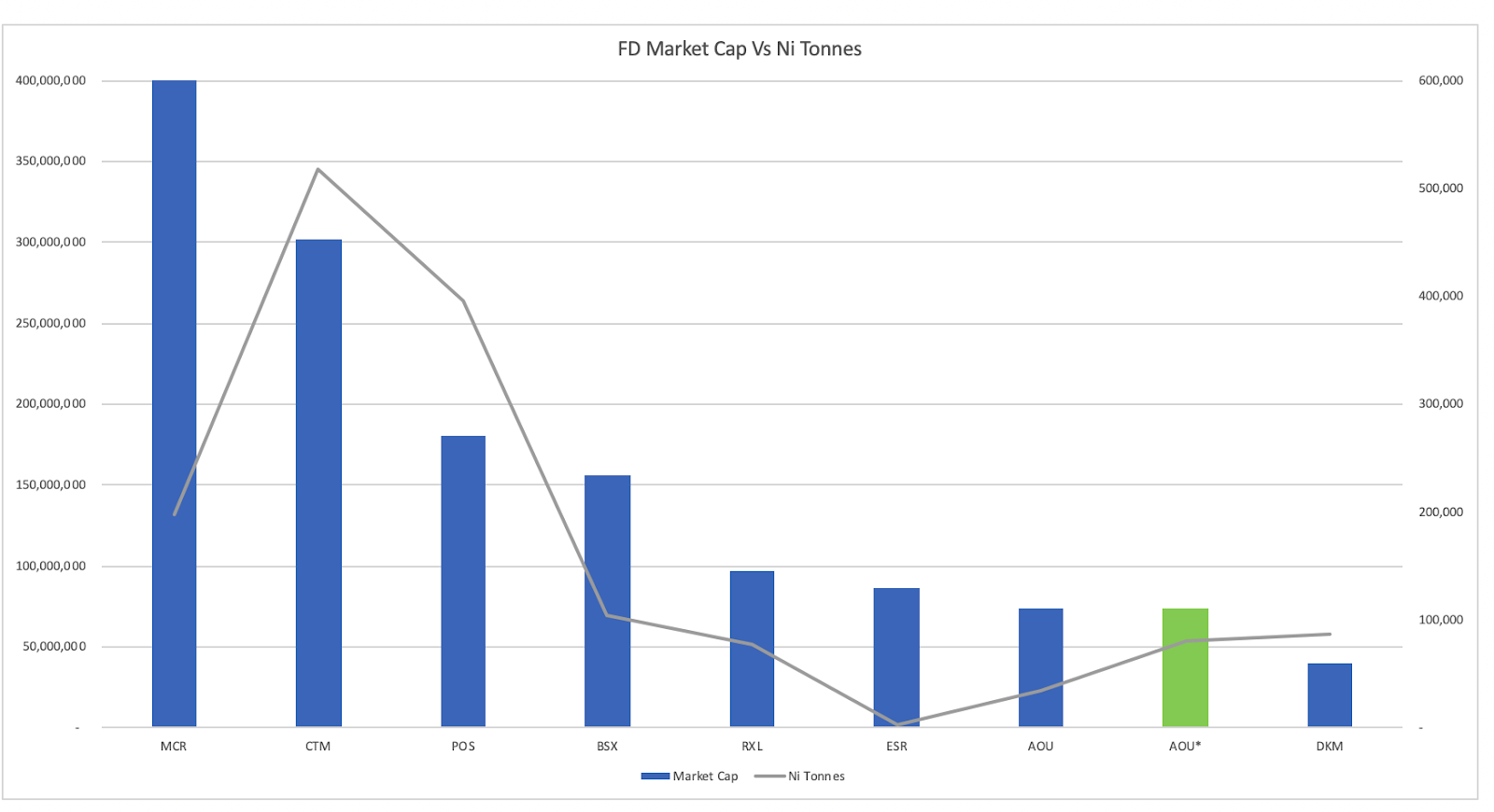

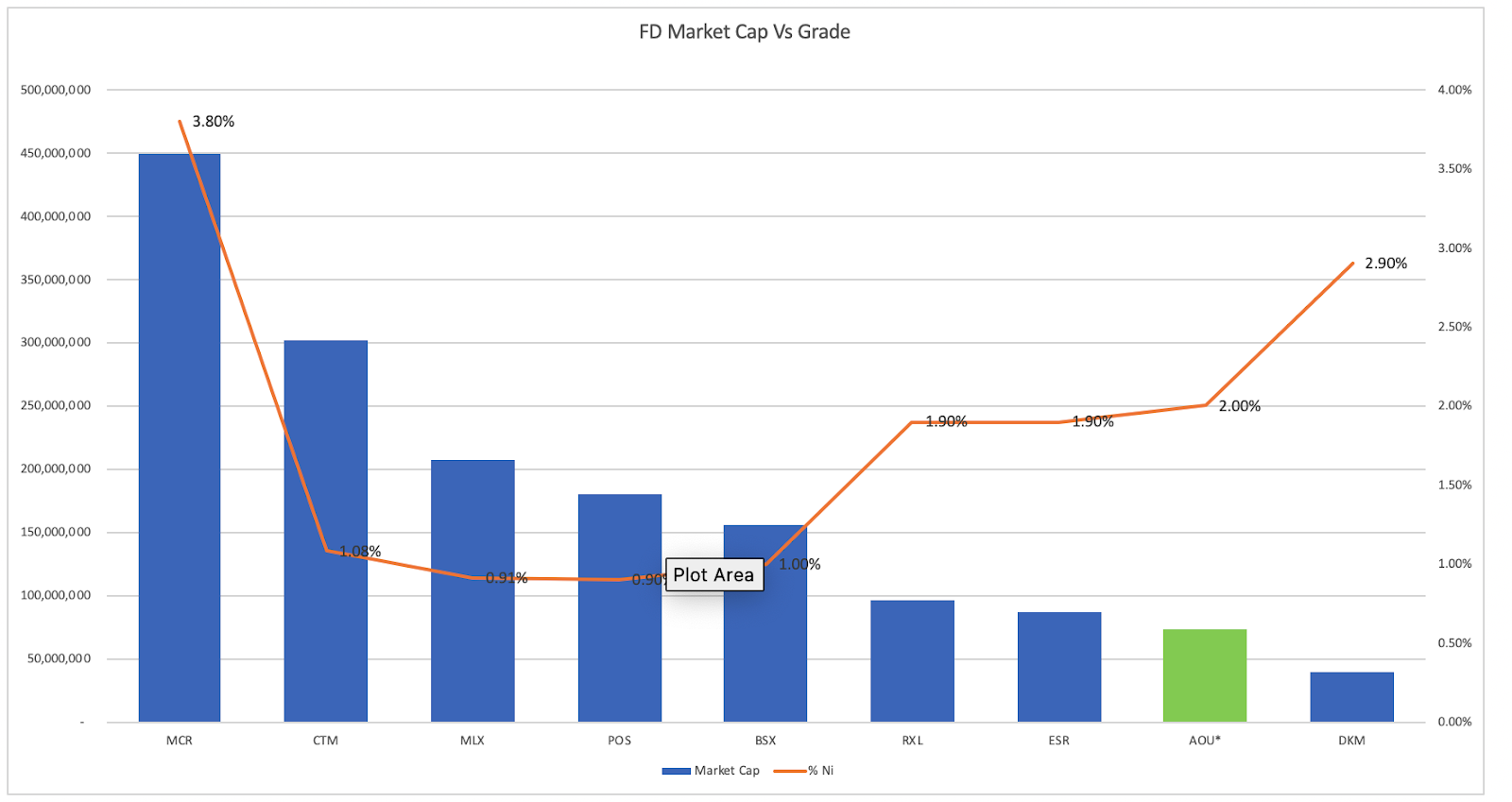

Relative to its sulphide nickel peers with commercial grades of 1% or higher (there are only a handful at 2% or higher), AOU would seem undervalued at $65M.

In fact, High grade nickel drill intercepts have seen Australian investors have a huge effect on nickel companies.

In October 1969, rumours of a significant high grade intercept saw Poseidon’s share price rise meteorically. On October 1 1969, Poseidon announced 40m at 3.56%. This saw the share price surge from $0.80 to a high of $280.

On 8 October 2020, ESR announced a 2.9m massive sulphide intersect and on 4 November the company confirmed assays of 2.5m at 3.66%. Its share price rose from 0.01 to 0.185 and its market cap soared to over $200m.

On 31 March 2020, Legend announced it had intercepted 12.8m of massive Nickel Sulphides. The share price rerated from 21 April on the back of assays of 12.8m at 2.78% Ni.

The share price rerated from 0.06 to 0.18 and the market cap hit close to $400M within a couple weeks.

On 9 November 2020, Azure announced assays of 3.9m at 2.85% Ni. Its share price rose from 0.32 to $1 and its market cap moved to above $300M.

Looking at AOU in comparison, It is capped at just $65M, but its historical drill core has shown results of 3m @ 11.78%. The share price is yet to recognise just how strong these results are. With plans to drill this target in the coming months, should AOU hit similar grades it could re-rate in line with its peers.

Here’s a look at how Auroch compares with its peers in terms of tonnage and grade:

Management has the runs on the board when it comes to discovering and developing world-class projects.

Chief executive Aidan Platel is a geologist with over 20 years’ experience in the minerals industry, traversing both mining and exploration roles across a wide range of commodities.

More recently, Platel has worked as an independent strategic consultant focusing on project evaluation, prior to which he spent 12 years in South America in mining and exploration.

He has a proven track record of exploration success having discovered and developed several major deposits including the world-class Santa Rita Nickel deposit which has contained nickel metal of more than 1 million tonnes. Santa Rita was commissioned by Mirabella which went from a penny stock to a multi-billion market cap.

Non-Executive Director Trevor Eton was as CFO and Company Secretary of sulphide nickel producer, Panoramic Resources Limited (ASX: PAN) from 2003 to 2020 in which he was instrumental in the financing, construction and development of the Savannah Nickel Project and the acquisition and subsequent development of the Lanfranchi Nickel Project, which saw the company reach a market capitalisation exceeding $1 billion in 2007.

Prior to Panoramic, he held corporate finance roles with various other resource companies, including diversified metal producers, MPI Mines Limited (MPI) and Australian Consolidated Minerals Limited (ACM).

Having Mr Eton on the team shows how serious AOU is about its nickel selling strategy, with his experience in negotiating offtakes with nickel buyers set to come to the fore.

With the acquisition of the Saints and Leinster Projects in late August 2019, AOU narrowed its focus to nickel exploration in the Norseman-Wiluna Greenstone Belt, arguably the best address globally for nickel sulphide mineralisation and home to numerous tier-1 nickel projects.

The acquisitions of the Saints and Leinster projects was perfectly timed as nickel enjoyed a remarkable resurgence, buoyed by a combination of supply pressures, local high-profile acquisitions and discoveries, Tier-1 production restarts and the EV demand juggernaut.

As stated, to support its exploration activity, AOU boosted its geological team.

The strategy bore immediate results with an updated geological model for the Saints project and significant aircore (AC) drilling programmes generating a stream of new basal channel targets (T1-T6), which have the highest probability of hosting thick zones of high-grade massive nickel sulphides and are extremely important for Kambalda-style komatiitic nickel sulphide deposits.

In the last six months, AOU has received promising assay results from its maiden diamond drilling program at the Horn Prospect, part of the Leinster Nickel Project.

AOU has flagged a planned drilling campaign at the Horn prospect to commence this month, which is expected to generate additional understanding of the potential here.

Most recently, massive sulphides were delineated within a larger mineralised interval of about 5 metres grading more than 2% nickel and 0.6% copper from the first hole.

The second hole (HNDD002) confirmed thick shallow high-grade nickel-copper-PGE sulphide mineralisation, with the logged massive sulphides interval reporting 7.3 metres at 2.2% nickel, 0.53% copper and 0.64 g/t palladium from 143 metres.

This hole has been very informative for AOU, as it also intersected the massive nickel sulphide mineralisation 15 metres further north along strike from an historic intercept of 14.7 metres at 2.19% nickel and 0.48% copper, effectively extending the mineralisation where previously it was thought to have terminated.

Hole HNDD003 returned a significant intercept of 1.5 metres at 1.5% nickel, 0.4% copper and 0.3 g/t palladium from 135 metres, including a smaller zone of massive sulphides grading 2.4% nickel and 0.5% copper.

However, it wasn’t so much the quality of the grades that were under the spotlight with this hole as it was drilled to test a historic drill hole electromagnetic (DHEM) conductor outside of the known mineralisation.

Consequently, intersecting massive sulphides at a relatively shallow depth is very encouraging in terms of assessing the quality of the data that to varying extents continues to shape exploration in the area.

DHEM surveys have been completed for all holes at the Horn and the geophysical data is currently being processed and modelled.

The results of the DHEM and the detailed geological logging will be used to plan the next stages of exploration at the Horn and surrounding prospects at Leinster.

The Saints Project has a Mineral Resources estimate of just over 1 million tonnes at 2.0% nickel and 0.2% copper for 21,400 tonnes of contained nickel and 1,600 tonnes of contained copper.

October 2019 drilling results featured some very strong nickel grades, most significantly 1.8 metres at 6.7% nickel and 0.27% copper, including 0.5 metres at 10% nickel and 0.24% copper.

Historical drilling results at this site also featured outstanding results over larger intersections such as 31 metres at 1.66% nickel and 0.16% copper, including 10.5 metres at 2.30% nickel and 0.25% copper.

The most recent drilling returned assay results of massive nickel sulphide mineralisation intersected in diamond drill-hole SNDD013.

The results came from the 1,200m diamond drill (DD) programme at the project.

The two main zones returned downhole intersections of 1.25 metres at 3.7% nickel and 0.18% copper from 241 metres, as well as a similar hit at the same depth within a broader mineralised zone of 3.7 metres at 1.85% nickel and 0.26% copper.

Prior to this drilling, there was a distinct lack of data to work with, but now that there are two very compelling drill targets for the next phase of diamond drilling management feels more confident that it can locate the feeder channel mineralisation within the Saints system.

AOU has transformed itself from a ‘drill and hope’ explorer across various disparate assets, to a nickel company that has a clear vision in terms of creating value through acquisitions, exploration, development and the negotiation of ore processing agreements.

The company’s assets are located in one of the best nickel regions in the world and it has a management team with global experience in discovering, developing and operating +1 million tonne nickel mines.

Under their stewardship it is expected that near-term production can be achieved at Nepean with the likelihood of a resource expansion, and exploration will also elevate the profile of the Leinster and Saints operations.

With five processing plants within trucking distance of AOU’s operations, the company does not have to deal with the traditional capital expenditure and logistical challenges faced by miners bringing new projects into production.

While commodity prices can be volatile, AOU’s exposure to the nickel price appears favourable given the metal’s seemingly attractive medium to long-term demand curve.

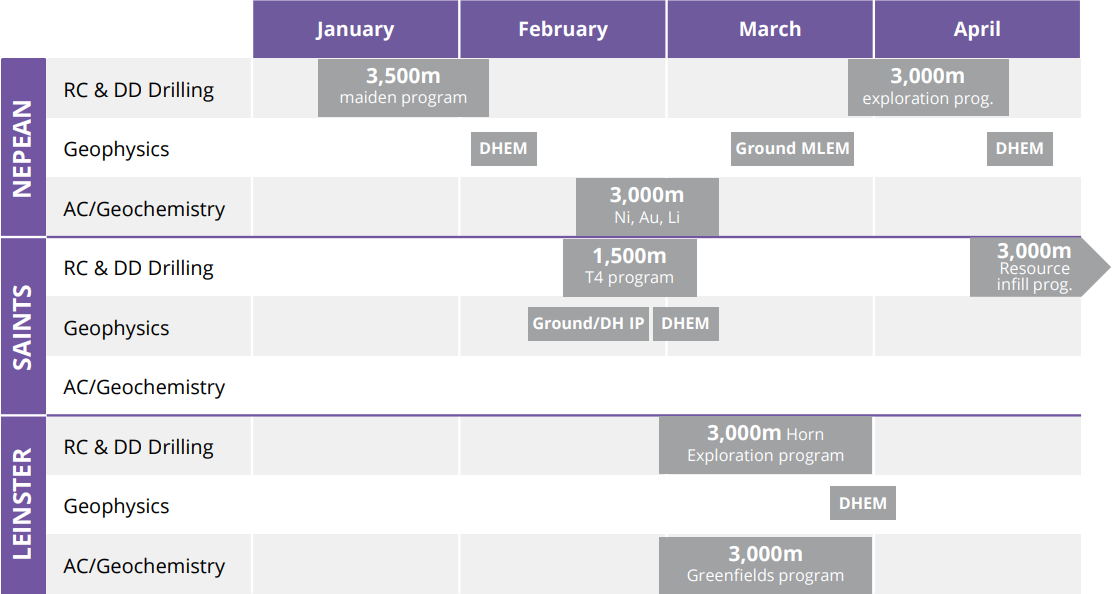

While the following table provides a snapshot of what has been delivered in recent months, and what to expect in the near term, AOU’s initiatives are likely to really come to the fore in the second half of 2021 as the company grows and officially establishes a much larger resource across the three assets.

The establishment of a combined resource, as well as the anticipated higher confidence levels that could be attributed to the Saints resource, will provide investors with the data to make peer value comparisons which are likely to indicate that an enterprise value-based share price rerating is warranted.

S3 Consortium Pty Ltd (CAR No.433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this report is general information only. Any advice is general advice only. Neither your personal objectives, financial situation nor needs have been taken into consideration. Accordingly you should consider how appropriate the advice (if any) is to those objectives, financial situation and needs, before acting on the advice.

Conflict of Interest Notice

S3 Consortium Pty Ltd does and seeks to do business with companies featured in its reports. As a result, investors should be aware that the S3 Consortium may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making any investment decision. The publishers of this report also wish to disclose that they may hold this stock in their portfolios and that any decision to purchase this stock should be done so after the purchaser has made their own inquires as to the validity of any information in this report.

Publishers Notice

The information contained in this report is current at the finalised date. The information contained in this report is based on sources reasonably considered to be reliable by S3 Consortium Pty Ltd, and available in the public domain. No “insider information” is ever sourced, disclosed or used by S3 Consortium.