Overview: Crowd Mobile Limited (“Crowd Mobile”, “the Company”) is an Australian technology Company focused on mobile software and services. The Company owns and operates a portfolio of trademarked software applications and messaging services for mobile devices, orientated toward the delivery of low-cost consumer advice. Founded in 2005, the Company has operations in 13 countries and has listed on the ASX via a reverse merger with Q Limited.

![]()

Catalysts: Crowd Mobile is poised to monetise recent distribution investments for its consumer advisory services. Historically restricted to delivery via Direct Carrier Billing (DCB) Premium SMS (PSMS), FY15 represents its first period with expanded capability utilising the app and web-based mechanisms. Service availability is also increasing from 13 to over 20 countries. Supported by a controlled cost base, near-term earnings growth stand as the primary driver.

Hurdles: Whilst the Company generates positive cash flow, its reliance on external capital remains to be eliminated. Existing revenue streams are predominantly derived from services distributed via PSMS and DCB, and there is no guarantee recent investments in new delivery techniques will be commercially successful. Demand for Crowd Mobile’s services is driven by consumer trends which can be transient and subject to limited-entry barriers for competitors.

Investment View: Crowd Mobile offers profitable exposure to the market for mobile software applications and services. We are attracted to its established income profile and scalability. Contingent on management’s cost control and marketing returns, our valuation represents a premium of 69 percent to a recent trade. Recognising the Company’s capital growth potential, we initiate coverage with a ‘speculative buy’ recommendation.

Crowd Mobile Limited (“Crowd Mobile”, “the Company”) is an Australian technology Company focused on mobile software and services. The Company owns and operates a portfolio of trademarked software applications (“apps”) and messaging services for mobile devices, orientated toward the delivery of consumer advice. Founded in 2005, the Company has operations in Australia, New Zealand, United Kingdom, Ireland, Germany, Austria, Italy, France, Belgium, The Netherlands, Hungary, Portugal, and Switzerland.

Crowd Mobile listed on the Australian Securities Exchange in January 2015, via a reverse merger with Q Limited. The listing coincided with a consolidation of Q Limited shares on a 1:40 basis and a $0.5million equity raising at $0.20/share (post-consolidation). The issued capital of the combined entity stands at $2million, or $0.028/share. Existing and new investors associated with Crowd Mobile accounted for 94.7 percent of shares in the combined entity.

Crowd Mobile’s primary asset is a portfolio of mobile software applications and messaging services orientated toward the delivery of consumer advice. The portfolio has been developed since 2005 and is supported by an integrated cloud-based management platform that allows the Company to service user demands utilising ‘crowd sourcing’ techniques (“Crowd Mobile Platform”).

Services provided by the Crowd Mobile Platform and its constituent applications are ‘question and answer’ orientated. Typically, consumers seeking advice on a particular matter send questions through one of Crowd Mobile’s service channels, for which the Company procures a rapid, relevant, tailored response.

The capacity to efficiently manage inbound questions and procure relevant responses is a critical feature of the Crowd Mobile Platform. During 2014, Crowd Mobile charged customers for over 3.4 million questions and internal testing of its technology platform has identified few capacity constraints to accommodate future growth.

Since its launch in 2008, the number of mobile software applications available in the Apple App Store has grown to 1.3 million. Consumption via the Apple App Store accounts for over half of the global apps market, which was estimated by Frost and Sullivan to be worth A$19.3 billion in 20131

App developers typically generate income by charging users a one-off fee, or via the provision of billable services within an otherwise freely available app (“freemium”). According to data compiled by Statista, under 10 percent of app downloads are paid, indicating that freemium models account for over 90 percent of the market by volume2. This market is dominated by game developers, with IBIS World estimating that over half of all apps are gaming apps3.

Crowd Mobile’s services fall under the ‘freemium’ category. Supporting applications are free to download, with the utilization of the service incurring charges on a ‘per question’ basis. In contrast to gaming apps currently dominating the market, Crowd Mobile’s services are oriented toward consumer advice. Services available cover consumer advice topics, including fashion, morals, and gossip.

Relative to gaming services which presently dominate the mobile apps market, Crowd Mobile’s business model appears less capital intensive and lower risk.

Freemium model with users incurring a fixed charge per service request

The ‘question and answer’ nature of its portfolio requires relatively low development and maintenance costs. The Crowd Mobile Platform manages order flow, whilst responses are generated by specialized contractors, remunerated on a ‘per answer’ basis. Crowd Mobile engages over 500 contractors located around the world answering in half a dozen languages. This operating structure ensures continuous “24/7” service availability and reduces fixed costs for the Company.

Moderators of the Crowd Mobile Platform can utilize a 51million question and response archive to accelerate service delivery, whilst features such as auto-correction and keyword matching maintain quality control between correspondences.

Analytical features of Crowd Mobile Platform allow the Company to identify changes in consumer trends and develop targeted services to complement its existing portfolio.

Crowd Mobile’s portfolio and distribution capability has historically been oriented toward PSMS services, which can be utilized by all mobile devices. However, in light of increasing smartphone adoption, the Company’s recent strategic focus has been the Crowd Mobile Platform. Cloud-based, versatile, and scalable – the Crowd Mobile Platform is capable of receiving questions from a variety mediums such as SMS, Web, and Apps.

Services now available via multiple delivery mechanisms

Advisory services currently provided via the platform are oriented toward fashion, morals, and gossip under the following trademarks;

– Passion for Fashion – Bongo – SMS Guru

– What Would Jesus Do – 63336 – Buddy

Expansion to 20 markets and low capex pipeline of new product rolls out to drive growth

Crowd Mobile’s initial focus is to expand these services with established demand profiles into new markets. Over the past 12 months, the Company has successfully expanded into non-English speaking markets and now operates in 13 countries. Plans are in place to be operating in over 20 countries within the next two years.

Concurrently, the Company is developing a pipeline of new products capable of delivering professional advisory services and relationship advice. Existing infrastructure associated with the Crowd Mobile Platform allows new services to be developed for low capital outlay.

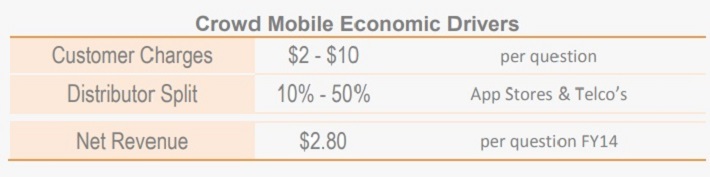

The cost of utilizing Crowd Mobile’s services typically ranges from $2 to $10 per question for the consumer. Crowd Mobile derives between 35% – 75% of these proceeds with the balance retained by distributors (telco and app stores). After deducting distributor splits, the Company generated revenue of $2.80 per question on average during FY14. Whilst most revenue was generated via PSMS services, the Crowd Mobile Platform has now removed this constraint.

With researchers paid a fixed split out of net revenue on a ‘per answer’ basis, the primary determinant of commercial success remains returns associated with marketing expenditure. The average user life cycle of Crowd Mobile’s services has historically been up to seven service requests, hence there is a need to constantly procure new users.

Return on marketing expenditure is the critical economic driver

Crowd Mobile conducts targeting marketing via social media and a joint venture with MTV. Its marketing strategy requires expenditure to be effectively ‘repaid’ via the first service requests generated by procured customers. Based on the Company’s existing fixed cost profile, and assuming that initial service requests ‘repay’ variable marketing costs, we estimate that customers become profitable after the 2nd question.

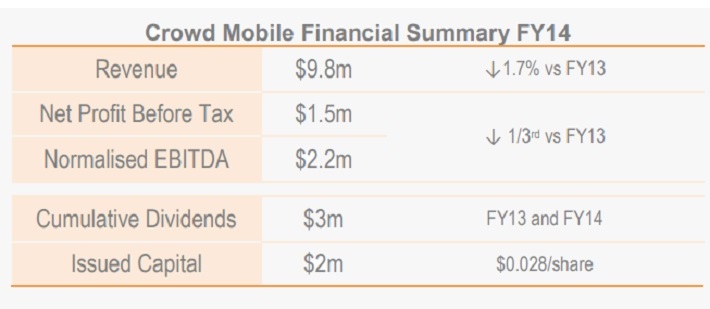

Crowd Mobile generates income via the provision of mobile software services and applications. A review of its operating history is limited to the last two financial years. Prior to its reverse merger with Q Limited, Crowd Mobile generated revenue of $9.8million, normalised EBITDA of $2.19million, and before tax profit of $1.5million during FY14.

FY14 before tax profit $1.5m

Against the previous corresponding period (pcp), revenue was largely flat, predominantly driven by PSMS services. Earnings contracted by approximately one third, related to increased marketing and software development expenditures associated with the Crowd Mobile Platform. The platform expands Crowd Mobile’s distribution capability beyond Premium SMS. Marketing and development costs are completely expensed in their year of occurrence.

Development costs completely expensed

Whilst the Company paid fully franked dividends totaling $3million during the past two years, we expect excess cash flow to now be reinvested for growth. Alongside retained earnings, Crowd Mobile has funded its growth strategy via a combination of hybrid securities and equity. To accompany its reverse merger with Q Ltd, Crowd Mobile issued new shares worth $2million at $0.20/share. Stock to the value of $0.3million was issued as consideration for existing convertible notes, $1million was issued in lieu of corporate advisory and director fees, whilst proceeds of $0.67million were raised from new shareholders with proceeds budgeted for working capital purposes. We estimate issued capital following the reverse merger and capital raise to be $2million, or $0.028/share.

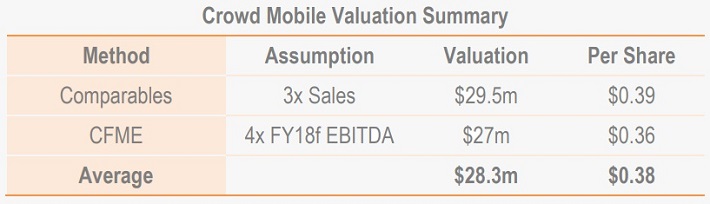

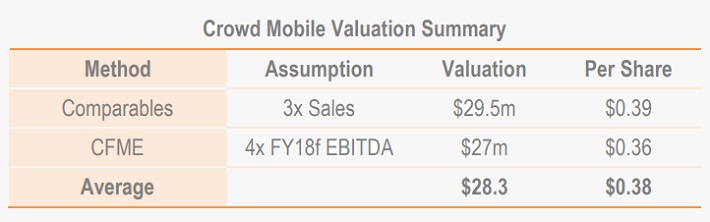

Crowd Mobile’s investment appeal rests in the current and future revenue streams generated by its portfolio of mobile applications and messaging services. We have considered the Company’s potential worth using a Comparables approach and Capitalisation of Future Maintainable Earnings (“CFME”) methodologies. Our appraisal is based on its current capital structure, hence assuming that no further external funding is required

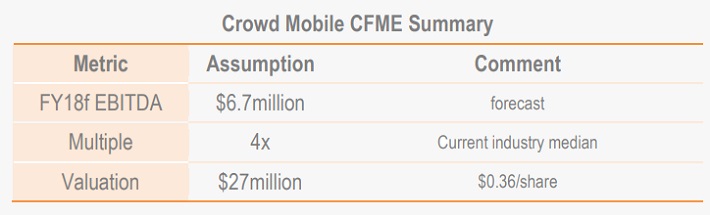

Valuation $0.38/share

Our Comparables approach arrives at a valuation of $29.5million, or

$0.39/share. Our CFME method arrives at a valuation of $27million, or $0.36/share Applying equal weightings both methods delivers an aggregate valuation of $28.3million or $0.38/share.

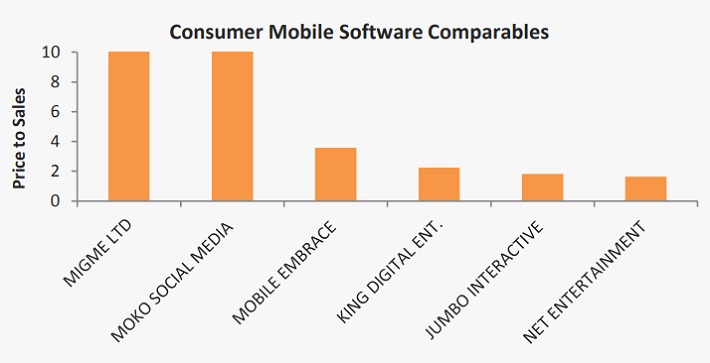

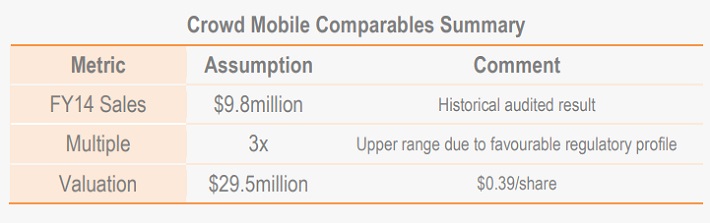

A universe of comparable companies has been assembled which are engaged in the provision of consumer-orientated mobile software services. Price to sales multiples ranges from 1.5 to 3.5 times FY14 revenue, with Moko Social Media (MKB.ASX) and Migme Ltd (MIG.ASX) notable outliers.

We note that companies engaged in mobile services incorporating gambling attract multiples at the lower end of the range, possibly due to the presence of greater regulatory burdens. As the advisory nature of Crowd Mobile’s services is subject to minimal regulation, we have applied a mid-range multiple of 3x, implying a valuation of $29.5million.

Sales multiples currently 1.5x to 3.5x

Post FY15, we have projected the Company’s financial performance for the next three financial years to a level that represents a sustainable earnings capacity. To our estimation of future maintainable earnings, an industry based multiple has been applied to arrive at a valuation of the Company.

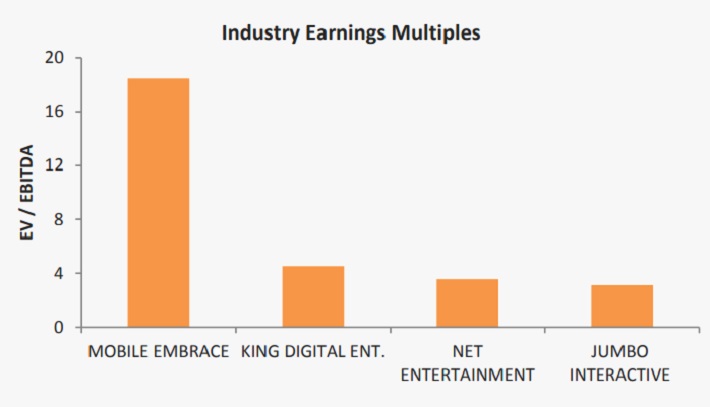

Median EBITDA multiple 4x

Our financial projections are based on the organic expansion potential of Crowd Mobile’s existing operations. We project EBITDA of $6.7million by FY18. Current industry trading multiples range from three to eighteen times EBITDA. Considering the relatively fewer data points for this approach, we have applied the median multiple of 4x to arrive at a valuation of $26million.

Crowd Mobile offers profitable exposure to the market for mobile software applications and services. We are attracted to its established income profile, scalability of the Crowd Mobile Platform, and near-term growth plans.

With limited entry barriers to competition and demand for its advisory services subject to consumer trends, returns on marketing expenditure are expected to be a critical determinant of the Company’s performance.

Valuation represents 69 per cent premium

Should management retain modest development costs and successfully execute their marketing strategy, earnings stand as Crowd Mobile’s primary share price catalyst. Our valuation represents a premium of 69 percent to a recent trade. Recognising the Company’s capital growth potential and unique existing cash flow profile, we initiate coverage with a ‘speculative buy’ recommendation.

Crowd Mobile relies upon relationships with aggregators and carriers in all markets it operates. These companies bill Crowd Mobile’s customers through their billing mechanism and pass on a share of the revenue to Crowd Mobile. A disruption in the relationship or technology may impair Crowd Mobile’s capacity to generate cash flow.

The Company’s income has historically been generated primarily through services delivered via Premium SMS. Whilst the Crowd Mobile Platform provides new capability to deliver service via multiple distribution mechanisms, consumer adoption is not guaranteed.

Crowd Mobile Services operate under regulatory codes and requirements that vary between jurisdictions and are subject to change. Imposition of greater regulations in one or more jurisdictions could add complexity and cost to the business, or even require key service features attractive to the majority of users to be disabled.

Intellectual Property protections surrounding Crowd Mobile’s assets are presently limited to trade marks and ‘know how’. There is no guarantee these protections will be sufficient to mitigate against competition.

Crowd Mobile’s long term growth strategy incorporates products orientated toward the provision of professional advice. Demand for the Company’s services in this field is untested.

Barriers preventing new competitors from entering the mobile services industry are generally low. Demand for software services of the nature currently supplied by Crowd Mobile may be subject to popular trends and change over time. There is no guarantee the Company can successfully adapt its product and service offering to in anticipation of popular trends.

Whilst Crowd Mobile generated positive cash flow during FY14, its earnings history is limited. There is no guarantee the Company will be able to execute its growth strategy without seeking external capital.

The Bulls Say

The Bears Say

Theo Hnarakis graduated from The University of South Australia with a Bachelor of Accounting and has held senior roles with News Corporation, Boral Group, the PMP Communications group, and was the Managing Director and CEO of Melbourne IT until 2013. He has also held director roles with Neulevel, a JV with US-based listed company, Neustar, and with Advantate, a JV with Fairfax Media. Mr. Hnarakis is also currently a Director of Newzulu Limited (ASX:NWZ).

Domenic has over 20 years’ experience developing and managing technology businesses. He co-founded and served as Group CEO of ASX-listed Destra Corporation Ltd (ASX: DES), which was the largest independent media and entertainment company in Australia with revenues of over A$100 million. Mr. Carosa was a director of Destra Limited until April 2009.

During the late ’90s Domenic lead the development of Australia’s leading digital music service provider for independent and unsigned artists – MP3.com.au – and founded Australia’s second-largest virtual web hosting/comms company which he sold for A$25 million in 2006-07. Domenic holds a Masters of Entrepreneurship & Innovation (MEI) from Swinburne University. Domenic is chairman of the Future Capital Development Fund, chairman of Dominet Digital Corporation Pty Ltd, an Internet investment group, and a non-executive director in Shoply Limited (ASX:SHP) and Collaborate Corporation Limited (ASX:CL8).

Mr. de Back has significant experience across multiple high-technology industries including mobile, gaming, and social media. He holds a master’s degree in corporate law from Amsterdam University. Mr. de Back is currently the Managing Partner at Incubasia Ventures, which is an unlisted investor and incubator working with innovative and scalable technology companies. He currently holds directorships for Moko Social Media (ASX: MKB) and iCollege (ASX: ICT).

Frank is an experienced finance professional with extensive profit- centre experience gained in several key accounting and management roles with major ASX and FTSE-listed companies. He specialises in restructuring and performance improvement, as well as mid-market merger & acquisition activities.

1. Frost and Sullivan (2014). Independent Industry Report on the Mobile Apps Market 2. Statista (2013). Mobile App Usage Dossier 3. IBIS World (2014). Smartphone App Developers in the US

S3 Consortium Pty Ltd (CAR No.433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this report is general information only. Any advice is general advice only. Neither your personal objectives, financial situation nor needs have been taken into consideration. Accordingly you should consider how appropriate the advice (if any) is to those objectives, financial situation and needs, before acting on the advice.

Conflict of Interest Notice

S3 Consortium Pty Ltd does and seeks to do business with companies featured in its reports. As a result, investors should be aware that the S3 Consortium may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making any investment decision. The publishers of this report also wish to disclose that they may hold this stock in their portfolios and that any decision to purchase this stock should be done so after the purchaser has made their own inquires as to the validity of any information in this report.

Publishers Notice

The information contained in this report is current at the finalised date. The information contained in this report is based on sources reasonably considered to be reliable by S3 Consortium Pty Ltd, and available in the public domain. No “insider information” is ever sourced, disclosed or used by S3 Consortium.