Overview: Crusader Resources Ltd (“Crusader”, “the Company”) is an Australian mining company focused on Brazil. It operates the Posse Iron Ore Mine (100%) in Minas Gerais state, cash flow from which is used to advance a portfolio of exploration to development stage gold and lithium assets. Crusader’s gold assets include the Borborema Project (100%), located in Rio Grande do Norte state, and the Juruena Project (100%), located in Mato Grosso state. The Company’s lithium asset is a Joint Venture (50%) incorporating the Manga Project, located in Goias state.

![]()

Catalysts: After securing a US$2million processing solution for Juruena, Crusader is rapidly advancing toward a decision to mine. Targeting a high-grade, open-pit / underground development, drilling is underway to convert existing resources to ‘indicated’ classification. Pending delivery of an Optimised Development Study at Borborema could reinforce this ‘sleeping’ asset’s long life ‘turn-key’ potential, whilst the planned ‘spin off’ of Crusader’s lithium JV is another driver in the current market conditions.

Hurdles: Whilst Posse mitigates Crusader’s capital demands, the Company remains reliant on external capital and there is no guarantee it can procure the additional funding required to develop its gold assets. With existing resources at Juruena classified as ‘inferred’ and independent feasibility studies yet to be concluded, there remains considerable uncertainty as to whether an economic mining operation can be established.

Investment View: Crusader offers speculative exposure to gold and iron ore markets through a diversified portfolio of operating and development assets in Brazil. Its track record of mine development, the scale of gold resources at Borborema, and near-term cash flow opportunity at Juruena is attractive qualities. Conversion of existing ‘inferred’ resources at Juruena into higher confidence categories and capital demands associated with Borborema are principal risks. With our valuation of $0.20/share representing a premium to recent trade, we are initiating coverage for Crusader’s ability to unlock value within its portfolio.

Crusader Resources Ltd (“Crusader”, “the Company”) is an Australian mining company focused on Brazil.

It operates the Posse Iron Ore Mine (100%) in Minas Gerais state, cash flow from which is used to advance a portfolio of exploration to development stage gold and lithium assets.

Crusader’s gold assets include the Borborema Project (100%), located in Rio Grande do Norte state, and the Juruena Project (100%), located in Mato Grosso state. The Company’s lithium asset is a Joint Venture (50%) incorporating the Manga Project, located in Goias state.

Crusader was incorporated in October 2003, and listed on the Australian Securities Exchange (“ASX”) in February 2004. Prior to June 2008, the Company’s name was Crusader Holdings NL. We estimate issued capital is currently $68million, or $0.29/share.

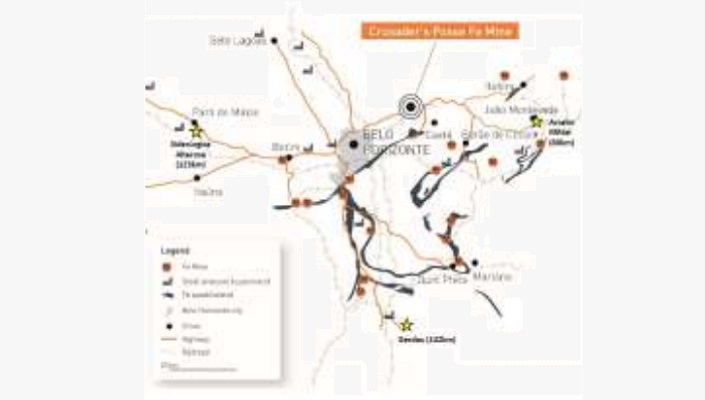

The Posse Iron Ore Mine (“Posse”, “the mine”) consists of one granted mining license, an open-pit mining operation, and a beneficiation plant in Minas Gerais state, approximately 30km from the capital, Belo Horizonte. The granted license (834.705/1993) covers an area of 1.09km2.

Crusader acquired Posse in September 2007 and advanced it from the exploration stage into an operating mine at a total purchase and development cost of $5.4million.

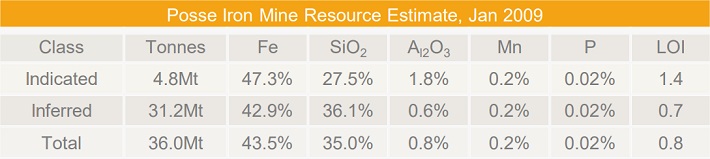

Posse has been in commercial production since March 2013. Reserves have not been certified. A resource estimate was prepared in January 2009, however, the estimate is not certified to current JORC (2012) reporting standards.

The output from the mine is marketed to a network of surrounding pig iron smelters, which make up Brazil’s “iron quadrangle”. A sealed highway network runs adjacent to the mine gate.

Since commissioning, we estimate the mine has generated free cash flow exceeding $10million and an internal rate of return exceeding 170 percent.

Crusader has utilised earnings generated by Posse to acquire and advance less developed assets within its portfolio.

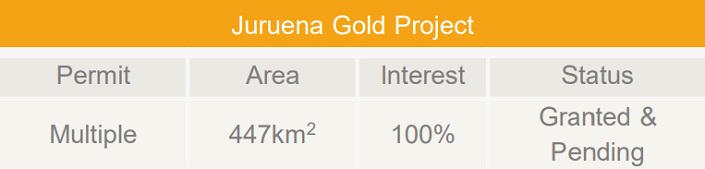

The Juruena Gold Project (“Juruena”) consists of 21 exploration licenses and applications located in the northwestern part of Mato Grosso state, near its boundaries with Pará and Amazonas states. The project covers 447km2 in a sparsely populated area. The small city of Alta Floresta is located some 250 km east-southeast of the property. Access is via dirt roads or light planes, with the site hosting a gravel airstrip.

Juruena was acquired in May 2014 from Lago Dourado Inc. (TSX:LDN) for $C650,000 plus 2million Crusader shares. All shares issued as part of the acquisition are subject to 12 months escrow, and 1.5million remain to be issued, contingent on development milestones.

The high grade Juruena Project is a near term cash flow opportunity

Artisanal miners have been active at Juruena since the 1970s, and it is estimated they have collectively extracted 0.5million oz gold. Prior to Crusader, two systematic exploration initiatives had taken place at Juruena since the 1990s, delivering ~44,000metres of drilling. Collectively these campaigns represented investment exceeding US$25million.

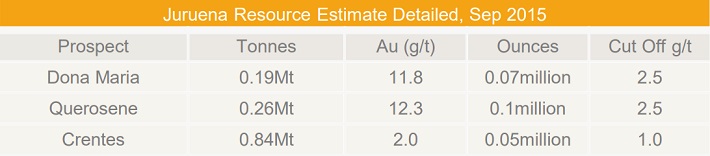

Subsequently, Crusader has delineated Juruena’s first certified resource estimate. Across three prospects Crusader has defined a JORC compliant resource of 0.23million ounces at an average grade of 5.6g/t, classified as inferred.

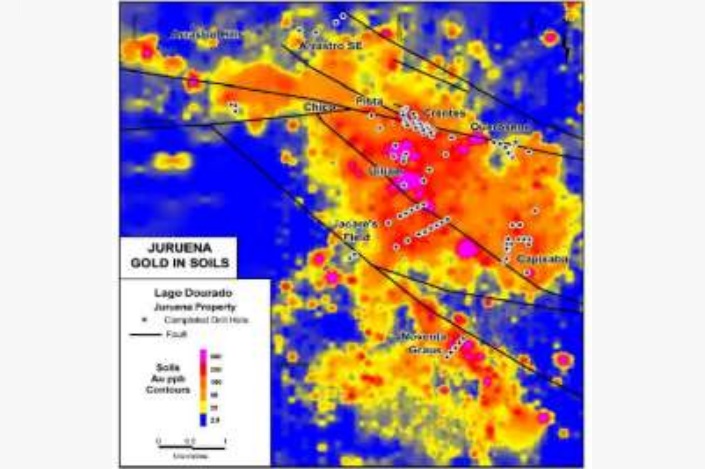

Juruena is situated on the western end of the prospective Juruena‐Alta Floresta Gold Belt, which is estimated to have produced ~7Moz from 40 documented discoveries since 1979. The main project area is centred around gold in soil anomaly spanning 8km by 4km, the style, and scale of which has been compared to Boddington (11Moz, Western Australia) and Las Cristinas (16Moz, Venezuela).

Whilst the scale of Crusader’s landholding and mineralised encounters to date may warrant investigation of Juruena’s potential to host large-scale gold projects, Crusader is presently focused on prospects capable of hosting a near-term, high-grade mine development.

Scoping study investigating a high grade open pit and underground mine development is nearing completion

A 10,000metre drilling program targeting close-to-surface ores formed the basis of a maiden 0.23million oz resource estimation in September 2015.

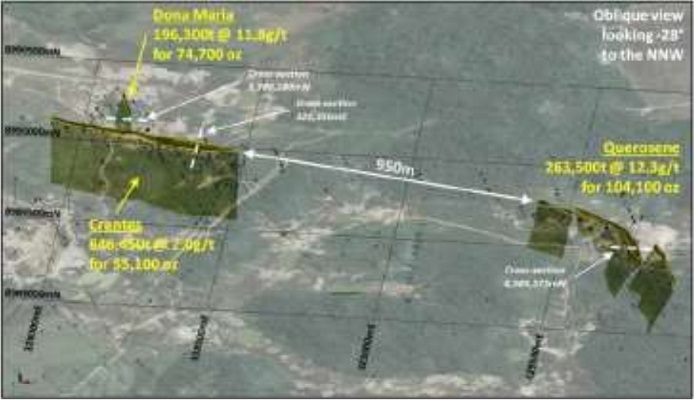

The resources are defined at three prospects within 1km of one another. A scoping study is currently underway to appraise the technical and economic merit of mine development, whilst applications for trial mining licenses have been lodged.

Maiden resource certified September 2015

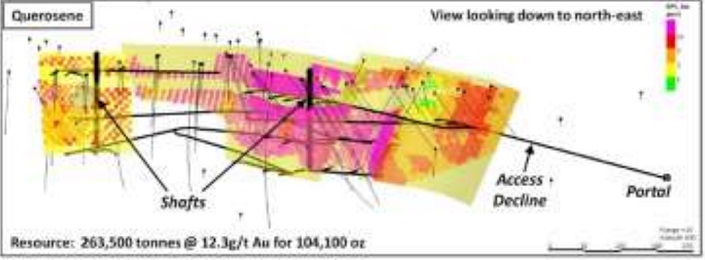

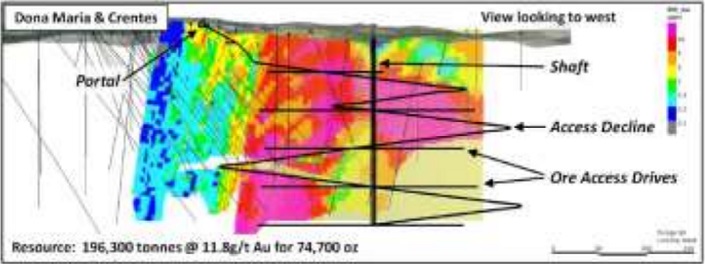

The scoping study is appraising open pit and underground mining scenarios involving two declines, at Dona Maria and Querosene. Completion, alongside an upgraded resource estimate, is scheduled for H1 2016.

Crusader is planning to develop Juruena as a high-grade, open pit and underground mining operation. Two declines, at Dona Maria and Querosene, are being considered as part of the current scoping study.

To support development, the Company has signed a non‐binding option to purchase and install a refurbished plant from Brazilian equipment supplier GNA (Minerales equipamentos e Acos Especiais Ltda).

Refurbished plant lowers upfront capex

GNA is an existing supplier of services and products to Crusader’s Posse mine. The plant includes three-stage crushing and a single ball mill recently purchased (second hand) by GNA. The option is for the supply and installation on-site at Juruena (turn‐key) and comes at a cost of ~US$2million.

Option secured over ‘turn-key’ processing plant for US$2million

The plant is capable of processing 0.1Mt pa and could support a production rate exceeding 30,000oz pa based on Juruena’s high grade, albeit ‘inferred’ resource component.

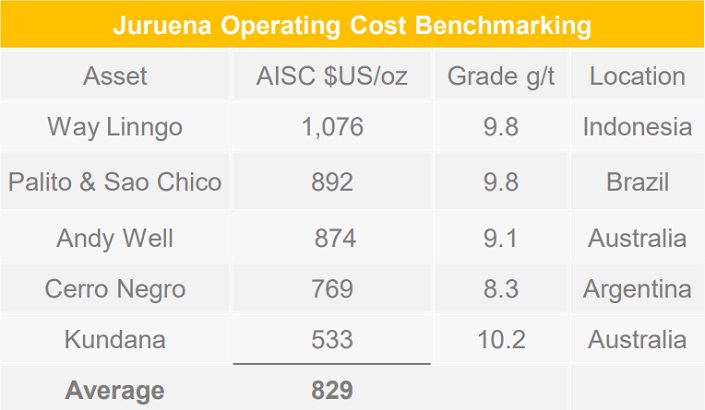

Whilst the Juruena Scoping Study remains subject to completion, we have benchmarked operating costs against similarly high-grade gold mines in Table 6.

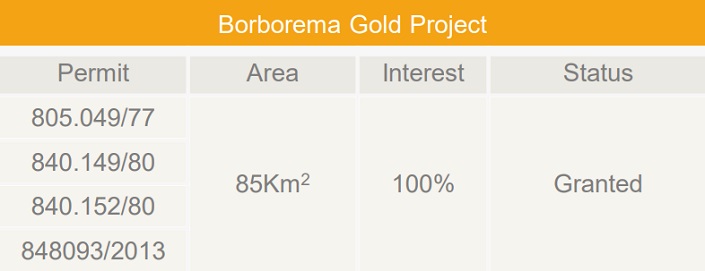

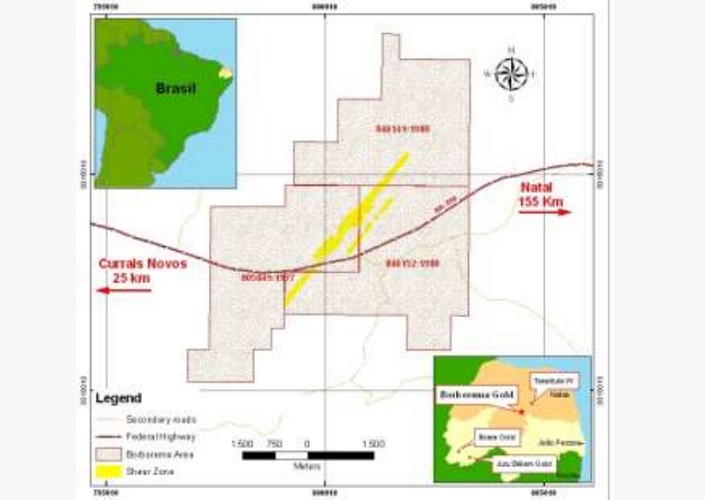

The Borborema Gold Project (“Borborema”) consists of 3 mining leases and one exploration license located in Rio Grande do Norte state. Borborema covers 85km2, approximately 155km from the state capital, Natal.

Borborema was acquired in August 2010 for $2.4million from privately held, MGP Ltda. It has excellent infrastructure with grid power, on-site water storage, established buildings, and bitumen road access. Natal hosts an international airport.

Artisanal miners had been active at Borborema since 1942. In 1984, the site hosted Brazil’s first-ever heap leach mining operation. Historic production is estimated to be 0.3million oz.

Borborema represents a long life ‘turn key’ opportunity

During 2007, prior to its acquisition by Crusader, Borborema was subject to a 75hole (~10,000metre) diamond drilling campaign which formed the basis of a non JORC compliant resource estimate.

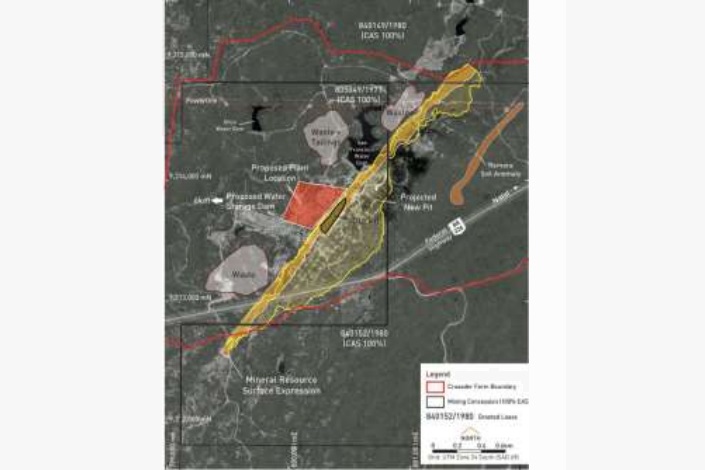

Since acquiring Borborema, Crusader has completed a Pre Feasibility Study into a 3Mt, 131,000oz pa mining operation, and delineated a proved and probable Reserve in November 2012 of 43.4Mt grading 1.18g/t for 1.6million oz. Note that the Reserve estimate is not compliant with the current JORC (2012) reporting standards.

After acquiring Borborema, Crusader investigated its potential to host a large-scale open-cut mining operation. The Company conducted over 40,000metres of drilling.

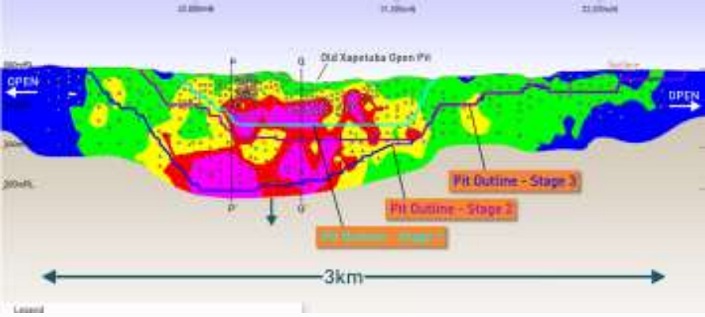

A Mineral Resource estimate was prepared in December 2011, however, this estimate is not compliant with current JORC (2012) reporting standards. The resources were estimated to depths of 350metres over a 3km strike and remained open in all directions.

These resource estimates formed the basis of a Pre Feasibility Study (“PFS”), concluded in September 2011, and subsequent Reserve estimate in November 2012, which is not compliant with current JORC (2012) standards.

Optimised Development Study, leveraging existing PFS and BFS works, is due for completion in H1 2016

A Bankable Feasibility Study (“BFS”) was initiated but later paused due to significant declines in the gold price. Subsequently, Crusader has commissioned an Optimisation Study to evaluate Borborema’s development potential under lower gold price scenarios, leveraging existing PFS and BFS materials.

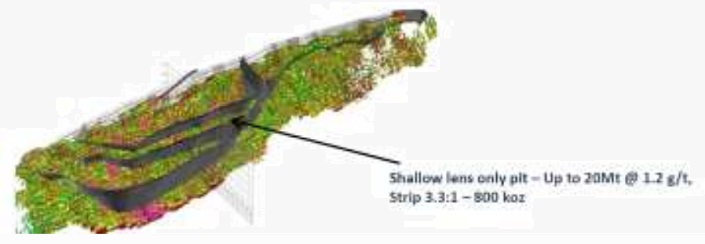

The Optimised Development Study is targeting a shallower Reserve (~0.8moz) than the November 2012 estimate, which is intended to reduce strip ratio, capital costs, and project footprint. The Optimised Development Study is scheduled for completion in H1 2016.

Optimised Development Study pending Completion

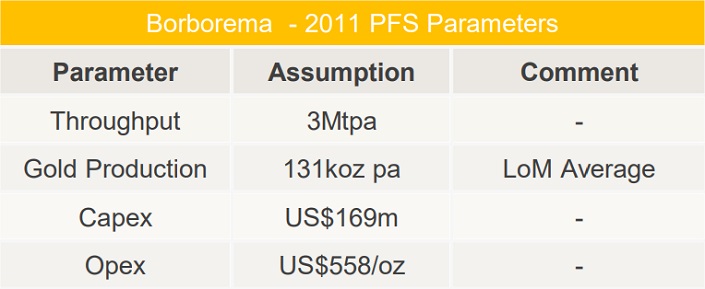

The 2011 PFS evaluated the technical and economic merit of a 3Mtpa open cut mining operation, producing 131,000oz pa on average over nine-year mine life.

The PFS was based on a Resource estimate which is not compliant with existing JORC (2012) reporting standards. Start-up capital costs were estimated to be US$169million, and operating costs to be $US558/oz. At a gold price of $1,300/oz, Crusader considered such an operation at Borborema as economically viable.

Optimised Development Study intends to demonstrate economics at lower gold prices

With gold prices trading significantly lower over recent years, Crusader has commissioned an Optimisation Study to ensure the development of Borborema is cyclically robust.

By focusing on the shallowest part of Borborema’s Reserve estimate, the Optimisation Study is expected to lower capital costs and the overall risk profile.

Optimisation Study is targeting a ~800,000oz Reserve

In addition, the Optimisation Study can account for recently favourable impacts stemming from a weakening in the Brazilian currency and global energy prices.

Crusader generates income from the Posse Iron Ore Mine. Since Posse’s commissioning in March 2013, the mine has generated cumulative revenue of exceeding $33million however income has not been sufficient to eliminate Crusaders reliance on external capital.

$6.25million placement in March

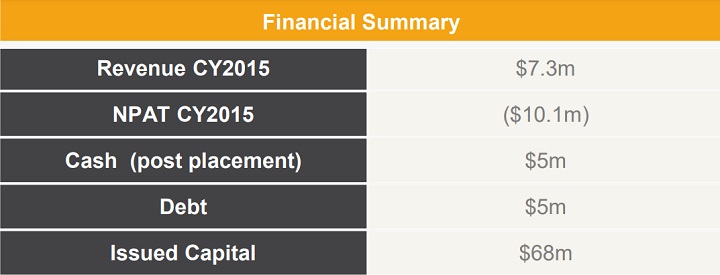

During 2015, Crusader reported revenue of $7.3million, a decline of 53 percent on the prior year due to weaker iron ore prices. Posse delivered a “break-even” result, with the Company reporting a gross profit of $0.05million, down from $6.2million in the prior year. Capital demands associated with other projects saw Crusader report a loss of $10.1million, which widened from a $4.1million loss in the prior year.

In addition to cash flow from Posse, Crusader has funded its capital demands via a combination of project debt and equity. As of March 2016, the Company’s borrowings stood at $5million.

The debt facility is supplied by Macquarie Bank and is secured over by a general security agreement over the assets of the Group, and a specific security agreement over the shares of the Australian subsidiaries. The facility bears an interest rate margin of 8.5 percent over the Bank Bill Swap Rate and matures 31st December 2016.

Crusader’s most recent equity financing initiative was a $6.25million placement at $0.10/share announced in March 2016. The placement expanded Crusader’s shares outstanding by 28.5 percent. Following the March placement, we estimate issued capital stands at $68million, or $0.29/share.

Crusader’s investment appeal rests in the near-term development potential of its Juruena Gold Project and “turn-key” optionality provided by Borborema.

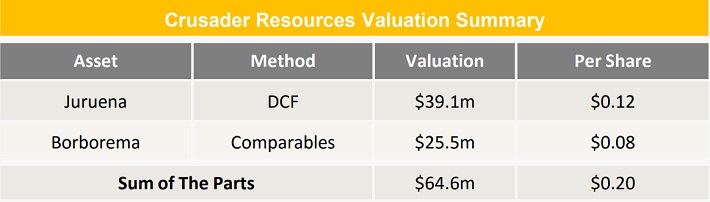

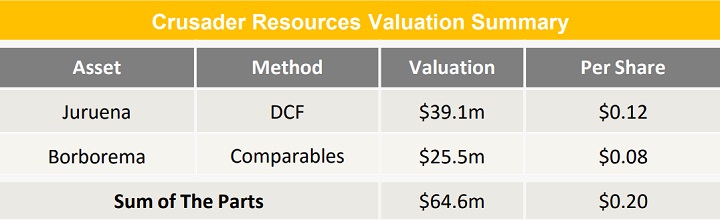

We have considered the Company’s potential worth using a Sum of the Parts (“SoTP”) approach, incorporating its Juruena and Borborema Gold Projects. It is assumed that surplus cash flow from Posse will be directed toward capital demands of Crusader’s gold portfolio, hence is implicitly accounted for in our funding forecasts. Crusaders other assets, including its Lithium Joint Venture – Third Element Metals Pty Ltd – are not incorporated into the valuation.

Valuation $0.20/share

Our appraisal is based on an expanded share count of 321.3million, reflecting an additional equity funding demand of circa $10million. We assume an AUD/USD exchange rate of 0.7 and take into account royalties but not corporate taxes.

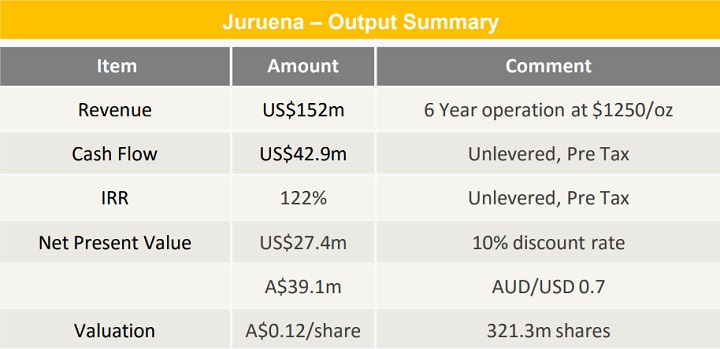

Our appraisal of Juruena utilises a Discounted Cash Flow (“DCF”) methodology and arrives at a valuation of $39.1million, or $0.12/share. Our appraisal of Borborema utilises a Comparables methodology and arrives at a valuation of $25.5million, or $0.08/share. Aggregating these estimates delivers a SoTP valuation of $64.6million or $0.20/share.

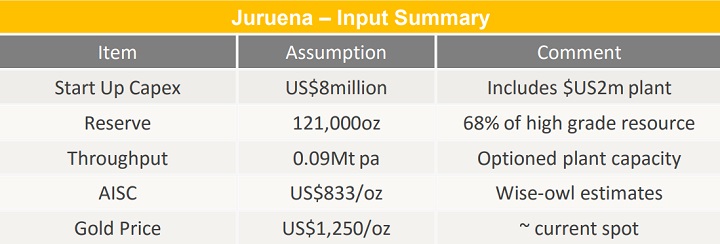

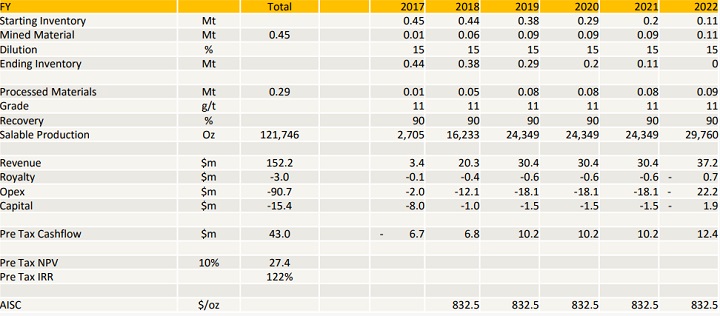

We have modeled a 5-6 year mining operation at Juruena focused on the current high-grade resource. It is assumed that 68 percent of the high-grade resource is recoverable. We have modelled a production rate of up to 30,000oz pa using a head grade of 11g/t.

Upfront capital demands are projected to be US$8million, with All In Sustaining Costs (“AISC”) averaging US$833/oz. Applying a US$1,250/oz gold price and a 10% discount rate yields a pre-tax Net Present Value of US$27.4million (A$39.1million, A$0.12/share).

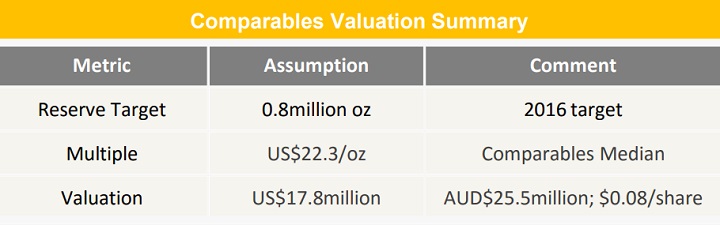

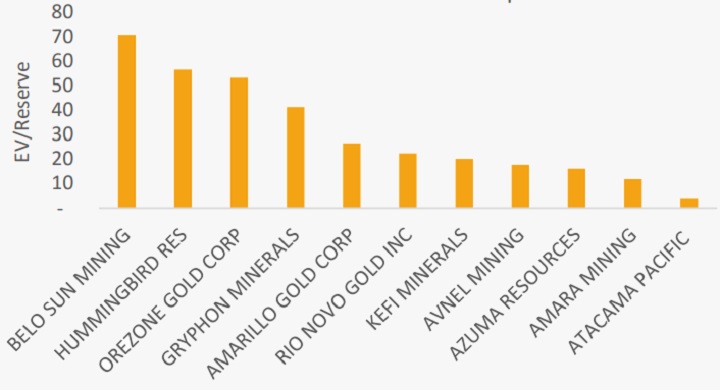

We have appraised the Borborema Gold Project utilising a Comparables methodology. A universe of comparable companies has been assembled which are principally engaged in the development of gold projects in developing jurisdictions of South America and Africa.

There are eleven relevant data points that have been considered based on their Proved and Probable Reserves. Valuations range between $5 and $70 per Reserve ounce.

Lithium assets not factored into valuation

We have utilised the 0.8million oz Reserve target incorporated into Crusader’s Optimisation Study and applied the median Comparable multiple of $22.3/oz to arrive at a valuation of US$17.8million (A$25.5million; $0.08/share).

Crusader offers speculative exposure to gold and iron ore markets through a diversified portfolio of operating and development assets in Brazil.

Its track record of mine development in Brazil, the scale of gold resources at Borborema, and near-term cash flow opportunity at Juruena is attractive qualities. The operating Posse mine mitigates capital demands across Crusader’s portfolio, whilst the Company’s recent $6.25million equity raising should provide sufficient funding to demonstrate the case for a mining development at Juruena.

Decision to mine at Juruena is a major driver

The Company’s ability to convert existing ‘inferred’ resources at Juruena into higher confidence categories, and secure the larger-scale capital required to develop Borborema are principal risks.

The planned spin-off of its lithium exploration joint venture presents a catalyst given current market sentiment towards these assets. Other drivers include a decision to mine at Juruena and delivery of the Optimised Development Study at Borborema.

With our valuation of $0.20/share representing a premium to recent trade, we are initiating coverage for Crusader’s ability to unlock value within its portfolio.

Mr. Copulos has over 30 years of experience in a variety of businesses and investments in a wide range of industries, including manufacturing, mining, fast food, property development, and hospitality. He has been the Managing Director of the Copulos Group of companies, a private investment group, since 1997. Mr. Copulos is an active global investor who brings significant business acumen and greater diversity to the Board of Crusader.

He has been a major shareholder of Crusader for many years and is aligned to improving shareholder returns. Mr. Copulos has over 14 years’ experience as a company director of both listed and unlisted public companies. He is currently the non-executive Chairman of Black Rock Mining Limited and was a non-executive director of Collins Foods until October 2014. Mr. Copulos is Chairman of the Remuneration Committee and a member of the Audit and Risk Committee.

Mr. Smakman is an Honours graduate of Monash University and has had a successful international career as a geologist and manager over the past 20 years. He has been associated with a variety of different commodities including gold, iron, uranium, copper, silver, and rare earths. He has held management roles in various countries and has served in senior public company management for several years. Mr. Smakman has been a resident of Brazil since 2006 and has negotiated the purchase of all of Crusader’s projects as well as managed their exploration, development, and operations.

Mr. Stephen holds a Bachelor of Commerce from the University of Western Australia. He has more than 20 years of experience in the financial services industry, starting as a portfolio manager at Perpetual Trustees in 1992 and working subsequently as a Private Client Advisor with Porter Western and Macquarie Bank. Mr. Stephen was a significant shareholder and Senior Client Advisor at Montagu Stockbrokers prior to their merger with Patersons Securities Ltd.

Mr. Rogers was the co‐founder of the highly successful Quantum Fund, which during 1970 ‐ 1980 gained 4200% while the S&P advanced approximately 47%. The Quantum Fund was recognised as one of the first truly international funds. In 1998, Mr. Rogers founded the Rogers International Commodity Index.

Mr. Rogers has a Bachelor’s degree in History from Yale University and a BA degree in Philosophy, Politics, and Economics From Oxford University. Since 1980, he has been an occasional guest Professor of Finance at the Columbia Business School.

Mr. Evans holds a Commerce (Hons) degree from the University of Queensland, is a Fellow of Chartered Accountants Australia & New Zealand, and is a member of both CPA Australia and the Australian Institute of Company Directors.

Mr. Evans is currently the Principal of a Business Broking and Advisory practice, and advises a broad range of businesses, in both the SME sector and larger corporate clients, on matters such as strategic planning, marketing, governance, and financial analysis. Prior to this, Mr. Evans held a series of executive positions in Finance and General Management in Australian public company groups over a 15 year period, in industries including telecommunications, banking and insurance, superannuation, and funds management, media, hospitality, and property development.

Mr. Ferreira is a senior executive with more than 35 years of experience in the natural resources and energy sectors. From 1986 to 2012, Mr. Ferreira held several positions within the Vale Group. He has managed distinct functions from exploration to sales and marketing in different businesses including iron ore, gold, fertilizers, kaolin, and energy.

In the early 1990s, Mr. Ferreira was actively involved in the exploration and development of three gold mines in Brazil. More recently he was Director of Special Projects in Sustainability and Energy, CEO of Vale Energia Limpa (Clean Energy), Director of Business Development at Vale Oil & Gas and Chief Executive Officer of PPSA Kaolim Mine and CADAM S.A. Mr. Ferreira earned a Bachelor of Science in Geology at Universidade Federal do Rio de Janeiro and attended the Ph.D. program at the University of Western Ontario. He has supplemented his experience with extensive executive education at Ibmec, University of Sao Paulo, Harvard University, Massachusetts Institute of Technology, INSEAD, and the International Institute for Management Development. Mr. Ferreira is a member of the Audit and Risk Committee.

Crusader has yet to certify Reserves compliant with current JORC (2012) reporting standards. Hence there are no guarantee existing mining operations at Posse can be sustained, or that the Company’s gold development projects can be economically mined. Resources presently delineated as a Juruena are classified as inferred, a category based on limited geological evidence and sampling.

Gold and iron ore prices have witnessed several years of contraction. Continuation of the trend or failure of these markets to recover could impair the economic value of mining, exploration, and feasibility programs being implemented by Crusader.

The Juruena and Borborema Gold Projects require further permitting and approvals before mining operations can be established.

Whilst Crusader generates revenue from Posse, it remains reliant on external capital to advance the development of Juruena and Borborema. There is no guarantee the Company will be able to secure access to additional funding or on terms favourable for existing shareholders.

Key inputs driving our appraisal of Juruena are based on estimates which have not been verified via an independent feasibility study, and gold prices above their 52 week average. Whilst our valuation of Borborema is based on a multiple of Proven and Probable Reserves, the asset does not presently host a Reserve estimate certified to current JORC (2012) reporting standards. If Crusader’s Reserve target failed to materialise, our appraisal of Borborema would therefore be significantly impaired. The holding structure of Crusader’s assets within a diversified corporate portfolio may impair their ability to attract fair value.

The Posse Mine may require a disproportionate amount of management resources relative to its contribution toward shareholder value. Whilst the operation may mitigate Crusader’s funding demands – there is a risk of diluting capacity for more value accretive initiatives.

THE BULLS SAY

THE BEARS SAY

S3 Consortium Pty Ltd (CAR No.433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this report is general information only. Any advice is general advice only. Neither your personal objectives, financial situation nor needs have been taken into consideration. Accordingly you should consider how appropriate the advice (if any) is to those objectives, financial situation and needs, before acting on the advice.

Conflict of Interest Notice

S3 Consortium Pty Ltd does and seeks to do business with companies featured in its reports. As a result, investors should be aware that the S3 Consortium may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making any investment decision. The publishers of this report also wish to disclose that they may hold this stock in their portfolios and that any decision to purchase this stock should be done so after the purchaser has made their own inquires as to the validity of any information in this report.

Publishers Notice

The information contained in this report is current at the finalised date. The information contained in this report is based on sources reasonably considered to be reliable by S3 Consortium Pty Ltd, and available in the public domain. No “insider information” is ever sourced, disclosed or used by S3 Consortium.