This is why we invested in ASX: IRD

11 days ago, we announced our latest investment – Iron Road Resources (ASX: IRD).

Today we share our deep dive analysis on why we have invested in IRD for the long term.

IRD is our eleventh investment. We invested in IRD because iron ore is booming, IRD’s iron ore project is later stage with a realistic path to market and IRD seems to be relatively undiscovered by the investors for now.

Since our initiation note last week, IRD is up over 80%. Here is our deep dive analysis on why we invested in IRD:

Click here to read our new ASX: IRD deep dive analysis

IRD owns 100% of a multi-billion dollar iron ore project in South Australia that sits ~ 150km away from its part owned port development that will allow its iron ore to reach the market.

IRD’s port development also includes potential for a green hydrogen export facility.

We invested in IRD’s recent placement because we believe IRD is currently undervalued by the market given the stage of its project, the global appetite for iron ore and rising interest in the green hydrogen thematic.

If you are too busy to read the deep dive, here are the seven key reasons we invested in IRD:

1. Leverage off IRD’s past investment: IRD has spent over $170M since 2008 to get the company to where it is today. At its current $225M market cap we feel like we are getting in at a very good valuation at the right time as the iron ore price starts to run again.

2. Strong macro theme: We expect IRD will perform very well if the iron ore price strength will continue in the global post pandemic construction boom.

3. Realistic path to market: IRD has a port development project for shipping its iron ore, which is already well progressed since 2008 – IRD is in the right place, at the right time with an advanced project.

4. Institutional Backing: US Private equity firm Sentient Global Resources Funds owns 72% of IRD and has been a very long term holder – which means there aren’t many shares available free float on the market. Macquarie Capital is also on IRD’s register.

Co-investing alongside big, cashed up institutions makes us feel confident in the investment over the long term.

5. Cash in Bank: IRD is debt free and has a healthy cash balance following recent capital raises that brought in $16M at 21.5c – we participated in this most recent placement, and so did IRD’s Directors.

6. Unknown and undervalued: We like IRD because it’s currently one of the lesser known stocks we have seen on the ASX. IRD appears to have done very little promotion to gain new investors over the last few years, hence offering a good chance of share price upside as they start to roadshow the story.

7. Net Present Value: IRD’s most recent financial modelling of the iron ore project demonstrated a NPV of US$2.6BN at a high grade iron ore price (65% Fe) at US$120/tonne. The iron ore price is currently over US$200/tonne.

Click here to get our new ASX: IRD deep dive analysis

What to expect from Wise Owl

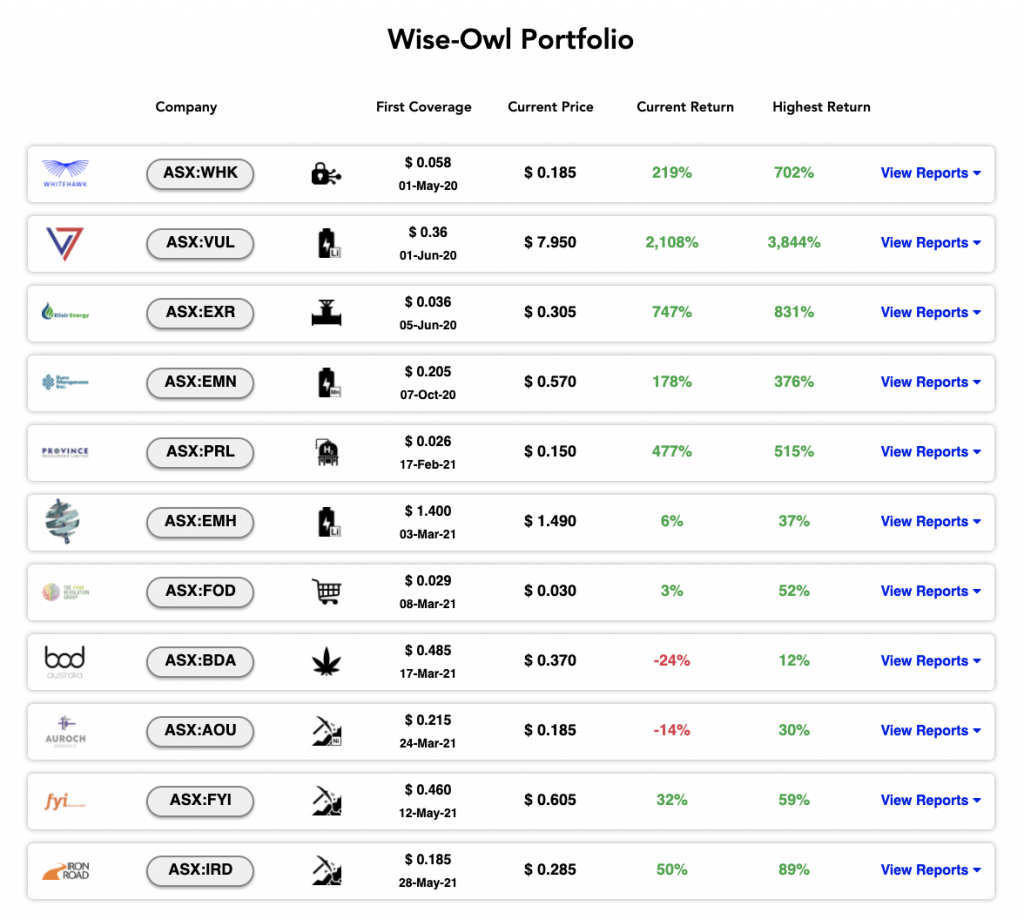

Wise Owl makes around ten long term investments per year in carefully selected ASX companies and we share our analysis on why we are invested and the companies’ progress over the long term. Here are our current investments:

We do extensive research and due diligence before we make a new investment. In our experience, holding companies for the long term, while they deliver on their business plans, has given us the best returns.

We send updates on all our investments as they evolve over time, and whenever we make a new investment.

Over the last 12 months we have made 10 investments in our portfolio.

IRD is our eleventh investment and you can see todays’ new “deep dive” analysis on why we invested here:

Click here to get our new ASX: IRD deep dive analysis

We look forward to bringing you more coverage on IRD over the coming months, starting with a today’s detailed research report:

Read Our Full Analysis