Overview: Analytica Ltd (“Analytica”, “the Company”) is focused on the design, development, and supply of low to medium-risk medical devices (Class I and IIa). Its most advanced product is the AutoStart® Burette – a next-generation FDA-approved hospital consumable. Currently, under development to treat women’s urinary incontinence, the PeriCoach® is a ‘mobile health’ consumer product scheduled to launch in 2014.

![]()

Catalysts: Manufacturing refinements undertaken during 2012 have attracted AutoStart® Burette marketing partnerships in Brazil and Taiwan. We now expect sales to be the critical value driver and were pleased to see Analytica’s Taiwan partner target a 10 percent market share within two years. Addressing an equally significant market, the PeriCoach® could become a company-making asset in its own right. Global shipments of mobile health devices are forecast to rise 16-fold by 2017. With the product launch scheduled for 2014, validation of the PeriCoach’s® commercial appeal offers additional growth potential.

Hurdles: Slower than forecast uptake of the AutoStart® Burette prompted Analytica to refine its design and manufacture. The lag has increased the Company’s reliance on external capital and could signal weak demand. The PeriCoach® requires further development and its commercial appeal has yet to be validated.

Investment View: Whilst engineering refinements have impacted sales, the AutoStart® Burette’s commercial potential remains significant. Having exercised cautious capital allocation whilst advancing a second product to market, we are confident in management’s ability to deliver shareholder value growth. After adjusting our forecasts for the AutoStart® Burette and appraising the new PeriCoach® technology, we value Analytica at $49.5m, or 7.6c/sh on a successful basis. Representing a premium of 260 percent to recent trade, we retain our ‘speculative buy’ recommendation.

Analytica Ltd (“Analytica”, “the Company”) is an Australian technology developer focused on commercializing low to medium risk medical devices (Class I & IIa). Its primary asset is Intellectual Property (IP) surrounding the market-ready AutoStart® Burette, and PeriCoach® Perineometer, currently under development.

The AutoStart® Burette is an advanced version of a common hospital consumable. The patented device is approved for sale in the US, European Union, and Australia, which Analytica aims to commercialise via royalty agreements.

The PeriCoach® is a consumer-oriented mobile health product currently under development designed to assist with the treatment of female urinal incontinence. It incorporates a patent-pending Perineometer device and mobile health software application.

Analytica listed on the Australian Securities Exchange in 2000 after raising $6m. Issued capital currently stands at $83.9 million, or 15c/share. Since acquiring the AutoStart® Burette technology in 2004, issued capital has increased by $6m, or 1c/share.

Analytica controls the rights to Intellectual Property (IP) surrounding the AutoStart® Burette – an advanced version of a commonly used medical device. Original patents surrounding the device were acquired in October 2004 for $60,000 in cash, 1 million shares, and a 4% royalty on net sales.

Analytica has subsequently re-engineered the device with an enhanced design incorporating fewer parts and lodged new patent applications in September 2012. A new patent has been awarded for China, with applications pending for the US, Australia, and Germany. Vendor royalty obligations expire after 2014.

In hospitals, care facilities, and emergency response vehicles, burettes are used to accurately measure the amount of medicine or fluid injected into patients intravenously (IV). The purpose of the burette is to avoid accidental fluid overload.

Normal burettes require manual refilling and can also suffer from irregular flow rates. Nurses often need to manually check the IV fluid as there is a risk of blood clots forming which may obstruct the intravenous cannula if the burette is unattended.

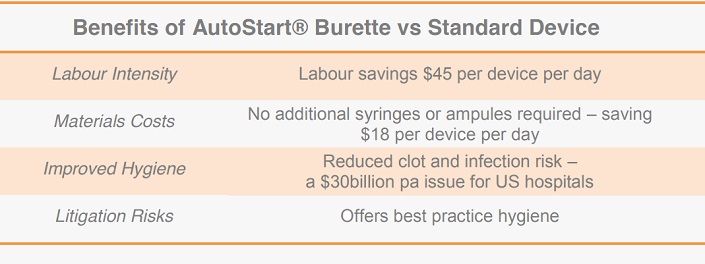

The AutoStart® Burette has four significant advantages over regular burettes; involving labour, material costs, hygiene, and legal risks.

By automatically refilling the IV fluid, medicine dosage flow from the device to the IV infusion bag becomes regulated, saving up to 20 minutes of nursing time per patient, per medication event. As average nurse wages in Australia are $45 per hour, and each patient may be medicated three times per day, the savings per burette may be up to $45/day. This represents seven times the cost of a standard burette.

The AutoStart® Burette’s flushing feature reduces the usage of other medical consumables as it allows for flushing with saline directly from the IV bag. Standard burettes require “flushing‟ with separate saline-filled syringes after IV drug delivery. As additional flushing syringes or ampules are therefore not required, the AutoStart® Burette can save an estimated $2.50 per medication event. This may save 6-8 ampoules or $18 per day.

Direct health benefits from the AutoStart® Burette include reduced blood clots and infection risk. Blot clot risk is reduced by automatically regulating the fluid flow to the patient, whilst the device’s flushing feature reduces the chances of bacterial contamination of the IV fluids, which can be fatal.

Equipment associated with intravenous fluid delivery such as stands and infusion pumps is some of the most common sources of bacterial contamination in hospital settings1. Infections contracted in hospitals are the fourth largest killer in America, adding an estimated US$30.5billion to the nation’s hospital costs each year2.

By offering best-practice hygiene, the AutoStart® Burette can also reduce litigation risks for hospitals, which cost the US health system US$3.6billion during 2012.

The AutoStart® Burette is approved for sale and distribution in the US, European Union, and Australia, with the US Food and Drug Administration (FDA) granting 510(k) clearance in March 2010.

Analytica’s target market is hospitals and standard burette suppliers. By engaging third-party distributors and standard burette manufacturers, the Company aims to receive a royalty on sales – reducing capital demands, production, and distribution risks.

To date, it has arranged distribution partnerships in Australia and Taiwan, whilst an agreement is being finalised in Brazil. Discussions have also commenced with a large multinational US-based supplier of medical devices, which recently concluded positive engineering appraisals of AutoStart® Burette.

As these offshore initiatives gather momentum, Australia represents the most developed marketing initiative involving the AutoStart® Burette. Whilst penetration has been limited, marketing has focused on hospital trials with feedback used to optimise the AutoStart® Burette for mass international markets.

Commercial trials have been implemented with three major Australian medical institutions – the New South Wales (NSW) Ambulance Service, Concord Repatriation Hospital, and an undisclosed hospital in Queensland. Concord Repatriation Hospital has subsequently entered a supply agreement expected to be worth $0.5m pa, although recent engineering and manufacturing enhancements have delayed its execution.

These supply chain adjustments saw manufacturing shift to an FDA-approved facility and amalgamation of the device’s features into one product rather than separate parts. They are expected to improve the AutoStart® Burette’s commercial appeal to global licensing partners.

We estimate the global market for burettes to exceed $3billion. Our calculations are based on the known spend of an Australian hospital per bed. They have been extrapolated globally after adjusting for differences in income and hospital bed count per capita.

The markets in which distribution partnerships have been established are estimated to be worth $340m. Whilst penetration has been limited in Australia, recent product enhancements have prompted Analytica’s Taiwan partner to target a 10 percent market share within 24 months of launch.

We estimate this level of success in Taiwan would generate royalties to Analytica around $1.5m pa. If replicated in global OECD nations, we estimate such market share would generate royalty income exceeding $60m pa.

The PeriCoach® is a consumer-orientated mobile health product used to treat female urinary incontinence. It incorporates a Perineometer treatment device and supporting mobile health applications for condition monitoring. Analytica controls all IP associated with the PeriCoach®, and accompanying ‘mobile health’ data applications.

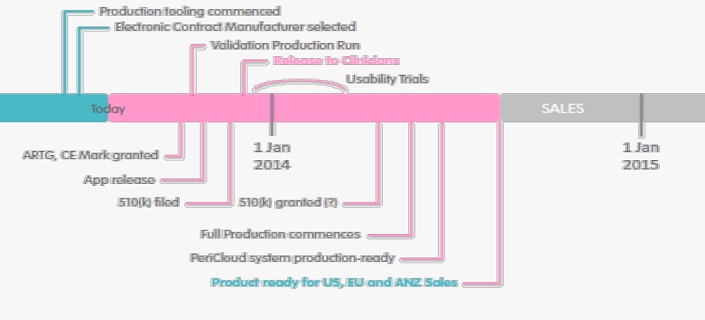

After overseeing its development for the past four years, Analytica is presently in the process of securing international patent protection and will soon commence the regulatory approvals process.

Studies indicate that a third of women suffer from urinary incontinence. The strength of the pelvic floor muscles plays a key role in managing this condition. Whilst training this muscle group through targeted exercises is the most common treatment method and can be extremely effective, difficulty engaging the correct muscles is a major barrier to success.

Devices known as Perineometers are available to assist with pelvic floor exercises. These medical devices are inserted into the vagina to measure the strength of intravaginal pressure and provide feedback to the user.

However existing products tend to lack accuracy and are indiscreet. By not indicating muscle groups responsible for the contraction, existing products risk further deterioration of the condition and can introduce more problems such as a prolapsed organ.

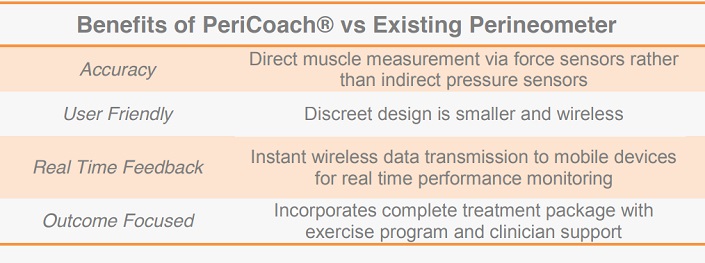

Analytica’s PeriCoach® technology has four key advantages over existing Perineometer devices. It is more accurate, user friendly, whilst accompanying mobile data applications provide transparent real-time feedback, with an outcome focus.

Improved accuracy is a core feature of the product’s design and IP. Existing devices use pressure sensors to indirectly measure pelvic floor muscle exercises. Whilst providing a general measure of vaginal pressure, this method does not indicate muscle groups responsible for the contraction.

The PeriCoach® utilises a patent-pending arrangement of force sensors that directly measure the effectiveness of pelvic floor muscles, overcoming risks associated with existing devices. Its design is also more user-friendly, being smaller, more discrete, and wireless.

Incorporating Bluetooth technology, the PeriCoach® provides its users real-time feedback regarding treatment. Performance data generated by pelvic floor exercises can be instantly transmitted to a mobile device, where accompanying software has been developed to provide audio and visual monitoring. The software forms a complete treatment package incorporating exercise programs and ‘cloud’ based data storage for later clinical appraisal.

The Continence Foundation of Australia estimates personal expenditures on urinary incontinence management products and laundry costs to be $191million. A recent similar study by Frost and Sullivan estimated the global incontinence market to be worth in excess of $5billion.

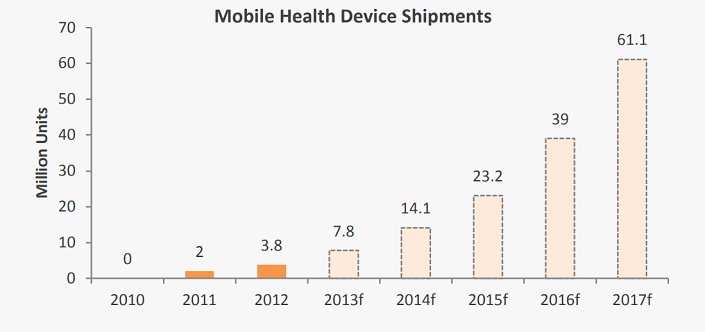

Analytica intends to market the PeriCoach® as a ‘mobile health’ package comprising the device and accompanying software. From a standing start in 2010, global shipments of mobile health devices were 3.8million units during 2012, and are expected to rise 16-fold by 2017.

After four years of development, Analytica has produced a prototype device and this year intends to register the PeriCoach® as a ‘class I’ (low risk) medical device in Australia and Europe, and ‘class II’ in the US. Staged marketing is scheduled from 2014. Whilst further patient trials are expected to establish usability, regulatory pathways are not considered onerous for products meeting ‘class I’ classification.

Distribution is planned through networks of specialist health practitioners such as physiotherapists and women’s health professionals.

Whilst the prevalence of urinary incontinence increases with age, mobility requirements associated with the PeriCoach® place women aged between 20-60 as the target demographic.

Over 6million Australian women fall in this age bracket. Applying a one in three prevalence rate yields a target market of 2million. Analytica aims to sell the PeriCoach® system for a total cost in the vicinity of $360 per user. With the Company seeking to adopt an in-house marketing and distribution strategy, we estimate that each one percent of the domestic market would generate net income exceeding $4.5m to Analytica.

The AutoStart® Burette is presently Analytica’s income-generating asset, however, for the last 18 months, it has not recorded sales due to a restructure of the product’s design and manufacture. The Company, therefore, remains reliant on external capital to maintain operations surrounding the AutoStart® Burette and commercialisation of its PeriCoach® IP.

To date, the Company has financed activities via equity and lines of credit. Issued capital currently stands at $83.9 million, or 15c/share. Since acquiring the AutoStart® Burette technology in 2004, issued capital has increased by $6m, or 1c/share.

Cash reserves stood at $0.3m as of June 30, supplemented by a presently unutilised $0.4m line of credit. The Company expects to receive a $0.52m Research and Development taxation incentive claim for the 2013 financial year and intends to conduct a Share Purchase Plan during the current quarter.

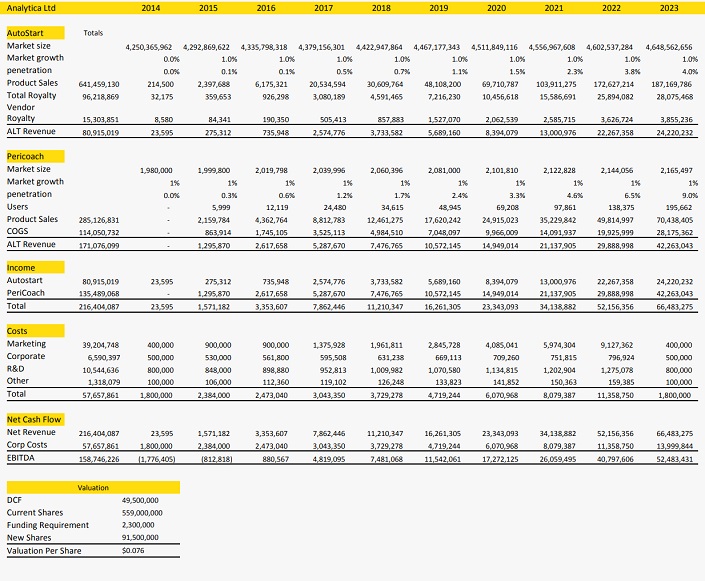

Analytica’s current investment appeal rests in its AutoStart® Burette and Pericoach® IP. We have appraised the Company using a Discounted Cash Flow (DCF) methodology.

Due to delays executing its agreement with Concord Repatriation Hospital and procuring additional contracts, we have revised market share projections that supported our existing Discounted Cash Flow model.

The impact of slower than forecast uptake of the AutoStart® Burette has been partly mitigated by our new appraisal of the PeriCoach®, After factoring in future funding requirements, we now value the Company at $49.5, or 7.6c/share.

We have projected Analytica’s potential cash flow from sales of the AutoStart® Burette and Pericoach® over a 10 year period ending 2023. The AutoStart® Burette has been appraised in a global context. Our analysis assumes the Company captures a 10 percent market share in regions where distribution partnerships have been established, and 3.5 percent in other OECD markets.

The model implies a peak global market share of 4 percent, peak product sales of over $187m pa, delivering revenue to Analytica up to $25m.

We have limited our appraisal of the Pericoach® to Australia. Our analysis assumes the Company captures a 9 percent market share, generating income to Analytica up to $42m pa.

We have maintained a 15 percent discount rate, yielding a net present value of $49.5 for the two technologies. While no further capital expenditures are anticipated to achieve these sales targets, we have factored in further equity raisings of $2.3m equity at an average price of 2.5c/share before the Company reaches a self-funding position.

With our sales forecasts being the primary risk factor in this model, we value Analytica at 7.6c/share.

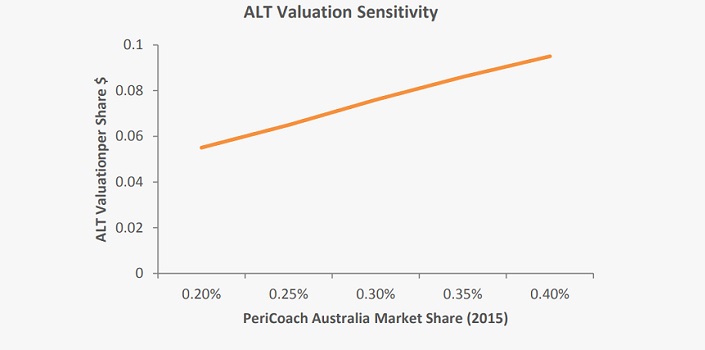

Our valuation is very sensitive to market penetration assumptions surrounding the PeriCoach, which constitutes 62.5 percent of our revenue projections over the forecast period. As can be seen in the chart below, each 0.05 percent change in initial (2015) domestic market share alters our valuation by 1c/share. We estimate that 0.05 percent market share corresponds to 1,000 unit sales.

Analytica is a speculative medical device company with performance linked to sales of its AutoStart® Burette and commercialisation of the PeriCoach®.

Since wise-owl initiated coverage in December 2011, the Company has successfully attracted international distribution partners and maintained disciplined capital management. We remain attracted to the AutoStart® Burette’s commercial potential, and management’s capital-efficient marketing strategy.

Whilst attributable to manufacturing adjustments undertaken during 2012, the lag in sales does carry a valuation impact. Risks associated with the delay are partly mitigated by the additional potential which the PeriCoach® now provides. The product could become a company-making asset in its own right, and success beyond the domestic market offers provides upside to our valuation.

Together, we appraise the AutoStart® Burette and PeriCoach® to be worth 7.6/share for Analytica. Representing a premium of 260 percent to recent trading levels, evidence of significant sales is required to realise this value and attracted to the balance of risks, we maintain our ‘speculative buy’ recommendation.

Our valuation assumes Analytica is successful in establishing a modest market share. If the Company achieves lower than forecast penetration or takes longer to achieve our targets, its valuation is likely to be significantly impaired.

Analytica’s commercialization strategy involves using third-party distributors and manufacturers. Third-party distribution agreements can stimulate buyer interest, but they do not guarantee sales as priorities between the parties may differ.

AutoStart® Burette sales are not yet sufficient to reduce Analytica’s reliance on external capital. There is no guarantee the Company will become self-funding, or successfully complete its current rights issue to pursue ongoing development activities.

The medicinal burette market is currently dominated by a few large medical device companies. It can often be difficult for a smaller company to break the stranglehold larger corporations have on an industry. Should Analytica be successful in capturing a small slice of the market the company may see itself as a takeover target before it can fulfill its true potential.

While management is large shareholders, the absence of cornerstone investors fosters instability for Analytica’s share register and impedes value growth in the event of commercial success. Should a takeover bid occur that does not reflect the value of its assets, the Company’s defences are limited, while a large number of shares outstanding hampers the stock’s ability to increase in price.

The Bulls Say

The Bears Say

Dr. Monsour is a medical practitioner with business interests in Queensland medical centres. He operates a medical management company that provides management support to medical practitioners and is also one of Australia’s leading providers of software systems for Occupational Health and Safety and Medical Accounting. Dr. Monsour is also chairman of Injet Digital Aerosal Ltd. Dr. Monsour was appointed to the Board in June 2004, becoming Chairman in 2006

Warren Brooks was the Managing Director and Founder of boutique Financial Advisory firm Clime AFM Pty Limited which was a wholly-owned subsidiary of Clime Investment Management Limited, an ASX listed company. Warren founded Australian Financial Management (Investment) Pty Limited in 1998 and sold the business to Clime Investment Management Limited in 2006. Warren previously had 28 year‟s experience working in Investment Banking and Stockbroking. Warren was appointed to the Board in July 2011.

Mr. Mangelsdorf is a Chartered Accountant with 32 year’s experience. He works with SME production, manufacturing, and retail firms assisting them with business, taxation, and management services, taking on the role of Chief Financial Officer for a number of firms. He is a director of a Queensland-based land development company and a chartered accounting firm. Mr. Mangelsdorf was appointed to the Board in 2010.

Mr. Daly is a Chartered Biomedical and Mechanical Engineer with over 16 years of professional engineering experience, the last thirteen in the medical device industry. He has an honours degree in Mechanical Engineering from the University of Queensland and an Executive MBA from the Australian Graduate School of Management in Sydney. Mr. Daly has expertise in design processes, quality systems, and business system improvement, and is trained in the use of Six Sigma tools. He has extensive hands-on design experience of product development in FDA QSR and ISO 13485 environments in some of Australia’s largest and smallest medical device companies. Mr. Daly was appointed as Operations Manager in 2005.

S3 Consortium Pty Ltd (CAR No.433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this report is general information only. Any advice is general advice only. Neither your personal objectives, financial situation nor needs have been taken into consideration. Accordingly you should consider how appropriate the advice (if any) is to those objectives, financial situation and needs, before acting on the advice.

Conflict of Interest Notice

S3 Consortium Pty Ltd does and seeks to do business with companies featured in its reports. As a result, investors should be aware that the S3 Consortium may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making any investment decision. The publishers of this report also wish to disclose that they may hold this stock in their portfolios and that any decision to purchase this stock should be done so after the purchaser has made their own inquires as to the validity of any information in this report.

Publishers Notice

The information contained in this report is current at the finalised date. The information contained in this report is based on sources reasonably considered to be reliable by S3 Consortium Pty Ltd, and available in the public domain. No “insider information” is ever sourced, disclosed or used by S3 Consortium.